在存在偏倚的情况下识别会计稳健性

IF 1.9

Q2 BUSINESS, FINANCE

引用次数: 0

摘要

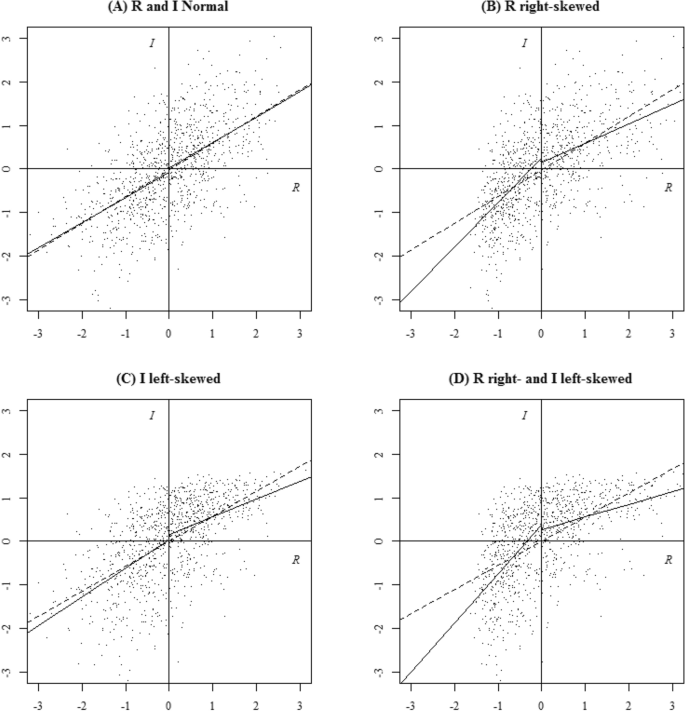

摘要不对称时效性(AT)系数作为会计稳健性的衡量标准一直备受争议。我们澄清了在存在偏度的情况下,AT系数识别会计稳健性的条件。具体而言,我们使用广泛的基于模拟的方法,研究了回报偏度、收益偏度和回报内生性的共同影响。我们表明,当收益是内生的时,收益和收益的偏度扭曲了作为保守性度量的AT系数。虽然收益偏度是条件保守性的预测结果,但回报偏度可以说与保守报告无关,不能通过简单的减少偏度的转换或离群稳健估计来解决。在经验上,我们分析了按规模和MTB排序的公司的AT和偏度,强调了跨群体恒定偏度对会计稳健性准确比较的重要性。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Identifying accounting conservatism in the presence of skewness

Abstract The asymmetric timeliness (AT) coefficient as a measure of accounting conservatism has been subject to much debate. We clarify the conditions under which the AT coefficient identifies accounting conservatism in the presence of skewness. Specifically, using an extensive simulation-based approach, we examine the joint impact of return skewness, earnings skewness, and return endogeneity. We show that skewness of returns and earnings distorts the AT coefficient as a measure of conservatism when returns are endogenous. While earnings skewness is a predicted consequence of conditional conservatism, return skewness is arguably unrelated to conservative reporting and cannot be tackled by simple skew reducing transformations or outlier-robust estimators. Empirically, we analyze AT and skewness of firms sorted on size and MTB, highlighting the importance of constant skewness across groups for accurate comparisons of accounting conservatism.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Review of Quantitative Finance and Accounting

BUSINESS, FINANCE-

CiteScore

3.20

自引率

17.60%

发文量

87

期刊介绍:

Review of Quantitative Finance and Accounting deals with research involving the interaction of finance with accounting, economics, and quantitative methods, focused on finance and accounting. The papers published present useful theoretical and methodological results with the support of interesting empirical applications. Purely theoretical and methodological research with the potential for important applications is also published. Besides the traditional high-quality theoretical and empirical research in finance, the journal also publishes papers dealing with interdisciplinary topics.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: