交易成本下金融市场的最优投资与消费

IF 1.4

2区 经济学

Q3 BUSINESS, FINANCE

引用次数: 0

摘要

我们考虑一个金融市场的投资组合优化问题,该问题由具有独立增量和跳跃的半鞅描述,并通过lsamvy过程定义。首先,对于功率效用函数,我们给出了相应的验证定理,然后以显式形式找到最优消费/投资策略。此外,在leland - lsametette方法构造的策略的基础上,我们发展了当投资组合修正次数趋于无穷大时交易成本为比例的金融市场的渐近最优投资与消费方法。最后,通过蒙特卡罗模拟对所得结果进行了数值说明。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Optimal investment and consumption for financial markets with jumps under transaction costs

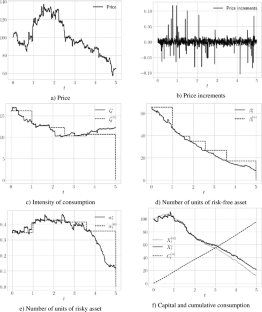

We consider a portfolio optimisation problem for financial markets described by semimartingales with independent increments and jumps defined through Lévy processes. First, for power utility functions, we show a corresponding verification theorem and then find optimal consumption/investment strategies in an explicit form. Moreover, on the basis of the strategies constructed using the Leland–Lépinette approach, we develop an asymptotic optimal investment and consumption method for financial markets with proportional transaction costs when the number of portfolio revisions tends to infinity. Finally, we provide Monte Carlo simulations to numerically illustrate the obtained results in practice.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Finance and Stochastics

管理科学-数学跨学科应用

CiteScore

2.90

自引率

5.90%

发文量

20

审稿时长

>12 weeks

期刊介绍:

The purpose of Finance and Stochastics is to provide a high standard publication forum for research

- in all areas of finance based on stochastic methods

- on specific topics in mathematics (in particular probability theory, statistics and stochastic analysis) motivated by the analysis of problems in finance.

Finance and Stochastics encompasses - but is not limited to - the following fields:

- theory and analysis of financial markets

- continuous time finance

- derivatives research

- insurance in relation to finance

- portfolio selection

- credit and market risks

- term structure models

- statistical and empirical financial studies based on advanced stochastic methods

- numerical and stochastic solution techniques for problems in finance

- intertemporal economics, uncertainty and information in relation to finance.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: