交易集群是否降低了交易成本?算法交易的周期性证据

IF 6

3区 经济学

Q2 BUSINESS, FINANCE

引用次数: 0

摘要

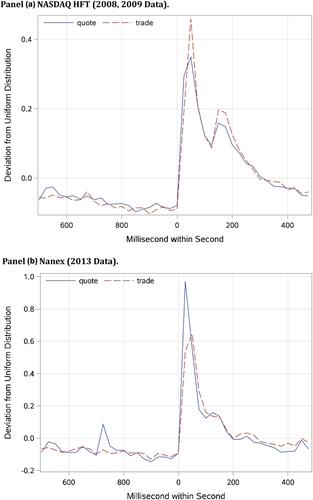

我们通过引入交易活动中的两个周期来研究交易活动如何影响流动性和波动性。首先,交易和报价更新在前100毫秒内比在其余时间内要频繁得多。其次,交易活动通常以一秒钟的间隔达到峰值。对于这两个周期,较高的交易强度和报价强度导致较高的波动性,但它们对股票流动性没有显著影响。这些周期性可能是由算法引起的,这些算法通过循环重复指令来预测交易,循环开始时间和时间增量。这种可预测的行为可能为交易算法中的行为偏差提供了一个例子。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Does trade clustering reduce trading costs? Evidence from periodicity in algorithmic trading

We study how trading activity affects liquidity and volatility by introducing two periodicities in trading activity. First, trades and quote updates are much more frequent within the first 100 ms of a second than during its remainder. Second, trading activity often spikes at intervals of exactly one second. For these two periodicities, higher trade and quote intensities lead to higher volatility, but they do not significantly affect stock liquidity. These periodicities are likely caused by algorithms that trade predictably by repeating instructions in loops with round start times and time increments. Such predictable behavior may provide an example of behavioral biases in trading algorithms.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Financial Management

BUSINESS, FINANCE-

CiteScore

6.00

自引率

0.00%

发文量

27

期刊介绍:

Financial Management (FM) serves both academics and practitioners concerned with the financial management of nonfinancial businesses, financial institutions, and public or private not-for-profit organizations.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: