{"title":"环境、社会和治理评级对偶发性股票风险的影响:未评级者、好者、坏者和罪人。","authors":"Matthias Horn","doi":"10.1007/s41471-023-00155-1","DOIUrl":null,"url":null,"abstract":"<p><p>This study analyzes whether stocks of companies with environmental social governance (ESG) rating show lower idiosyncratic risk. The main analysis covers 898,757 company-month observations of US stocks in the period from 1991 to 2018 and controls for stocks' exposure to liquidity, mispricing, innovations in volatility risk, investor sentiment, and analysts' forecast divergence. The main finding is that the receipt of an ESG rating decreases idiosyncratic stock risk. The effect is stronger for stocks that receive a higher ESG rating. Nevertheless, even when companies receive a lower ESG rating, they show significantly lower idiosyncratic risk than stocks without an ESG rating. Furthermore, stocks subject to a negative screen show lower idiosyncratic risk during recessions than comparable stocks with an ESG rating but without a negative screen. The results support the notion that the receipt of an ESG rating decreases uncertainty regarding future stock risk and return and show that ESG ratings and negative screens individually influence stock risk and, therefore, should be considered separately.</p>","PeriodicalId":74759,"journal":{"name":"Schmalenbachs Zeitschrift fur betriebswirtschaftliche Forschung = Schmalenbach journal of business research","volume":" ","pages":"1-28"},"PeriodicalIF":0.0000,"publicationDate":"2023-02-21","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9942038/pdf/","citationCount":"0","resultStr":"{\"title\":\"The Influence of ESG Ratings On Idiosyncratic Stock Risk: The Unrated, the Good, the Bad, and the Sinners.\",\"authors\":\"Matthias Horn\",\"doi\":\"10.1007/s41471-023-00155-1\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><p>This study analyzes whether stocks of companies with environmental social governance (ESG) rating show lower idiosyncratic risk. The main analysis covers 898,757 company-month observations of US stocks in the period from 1991 to 2018 and controls for stocks' exposure to liquidity, mispricing, innovations in volatility risk, investor sentiment, and analysts' forecast divergence. The main finding is that the receipt of an ESG rating decreases idiosyncratic stock risk. The effect is stronger for stocks that receive a higher ESG rating. Nevertheless, even when companies receive a lower ESG rating, they show significantly lower idiosyncratic risk than stocks without an ESG rating. Furthermore, stocks subject to a negative screen show lower idiosyncratic risk during recessions than comparable stocks with an ESG rating but without a negative screen. The results support the notion that the receipt of an ESG rating decreases uncertainty regarding future stock risk and return and show that ESG ratings and negative screens individually influence stock risk and, therefore, should be considered separately.</p>\",\"PeriodicalId\":74759,\"journal\":{\"name\":\"Schmalenbachs Zeitschrift fur betriebswirtschaftliche Forschung = Schmalenbach journal of business research\",\"volume\":\" \",\"pages\":\"1-28\"},\"PeriodicalIF\":0.0000,\"publicationDate\":\"2023-02-21\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9942038/pdf/\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Schmalenbachs Zeitschrift fur betriebswirtschaftliche Forschung = Schmalenbach journal of business research\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s41471-023-00155-1\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"\",\"JCRName\":\"\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Schmalenbachs Zeitschrift fur betriebswirtschaftliche Forschung = Schmalenbach journal of business research","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s41471-023-00155-1","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

The Influence of ESG Ratings On Idiosyncratic Stock Risk: The Unrated, the Good, the Bad, and the Sinners.

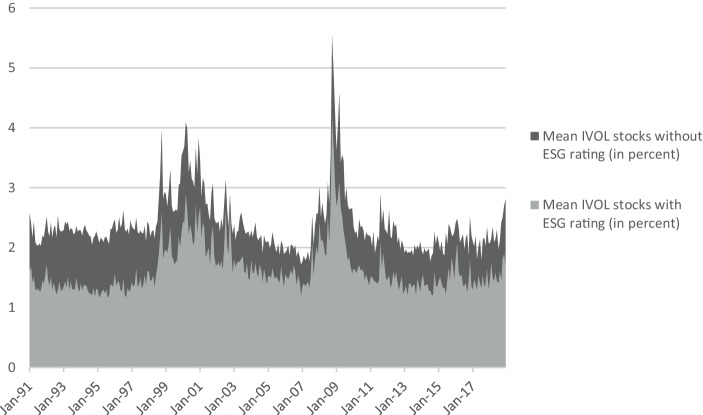

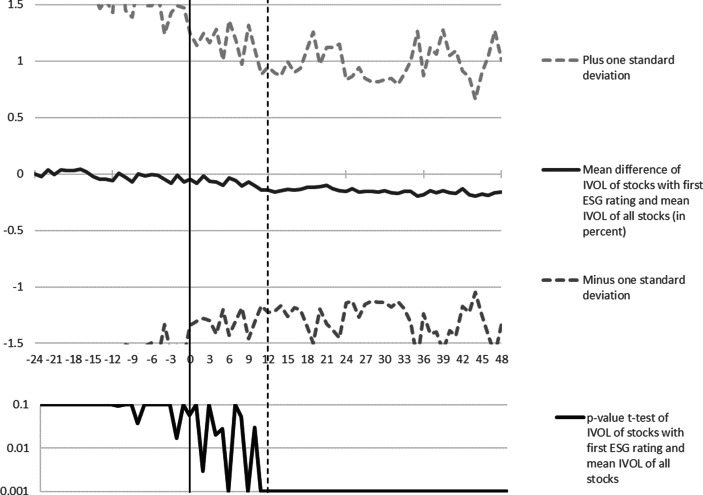

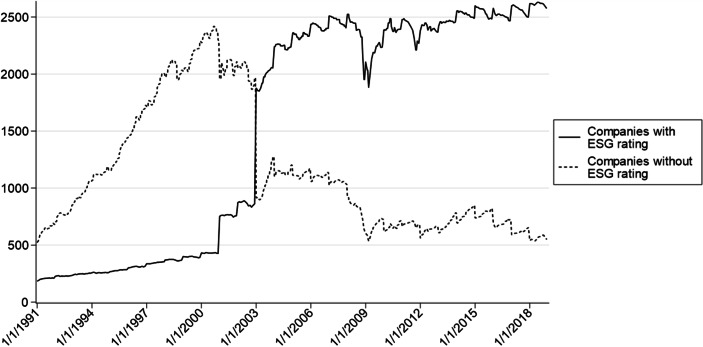

This study analyzes whether stocks of companies with environmental social governance (ESG) rating show lower idiosyncratic risk. The main analysis covers 898,757 company-month observations of US stocks in the period from 1991 to 2018 and controls for stocks' exposure to liquidity, mispricing, innovations in volatility risk, investor sentiment, and analysts' forecast divergence. The main finding is that the receipt of an ESG rating decreases idiosyncratic stock risk. The effect is stronger for stocks that receive a higher ESG rating. Nevertheless, even when companies receive a lower ESG rating, they show significantly lower idiosyncratic risk than stocks without an ESG rating. Furthermore, stocks subject to a negative screen show lower idiosyncratic risk during recessions than comparable stocks with an ESG rating but without a negative screen. The results support the notion that the receipt of an ESG rating decreases uncertainty regarding future stock risk and return and show that ESG ratings and negative screens individually influence stock risk and, therefore, should be considered separately.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: