{"title":"避税地和跨境许可与转让定价监管。","authors":"Jay Pil Choi, Jota Ishikawa, Hirofumi Okoshi","doi":"10.1007/s10797-022-09770-w","DOIUrl":null,"url":null,"abstract":"<p><p>Multinational enterprises (MNEs) have incentive to reduce tax payment through transfer pricing. The incentive is stronger when MNEs own intangibles, because it is easy to transfer them across countries. To mitigate such strategic tax planning, the OECD proposes the arm's length principle (ALP). This paper deals with technology patents as an example of intangibles and investigates how the ALP affects MNEs' licensing strategies and welfare in a model with a tax haven. The ALP may distort MNEs' licensing decisions, because providing a license to unrelated firms restricts MNEs' profit-shifting opportunities due to the emergence of comparable transaction. Interestingly, the termination of licensing in the presence of the ALP may worsen domestic welfare if the (potential) licensee and the MNE's subsidiary do not compete in the domestic market but may improve welfare if they compete. The results under ad valorem royalty are in distinct contrast with those under per-unit royalty.</p>","PeriodicalId":47518,"journal":{"name":"International Tax and Public Finance","volume":" ","pages":"1-34"},"PeriodicalIF":1.4000,"publicationDate":"2022-12-06","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9734996/pdf/","citationCount":"0","resultStr":"{\"title\":\"Tax havens and cross-border licensing with transfer pricing regulation.\",\"authors\":\"Jay Pil Choi, Jota Ishikawa, Hirofumi Okoshi\",\"doi\":\"10.1007/s10797-022-09770-w\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><p>Multinational enterprises (MNEs) have incentive to reduce tax payment through transfer pricing. The incentive is stronger when MNEs own intangibles, because it is easy to transfer them across countries. To mitigate such strategic tax planning, the OECD proposes the arm's length principle (ALP). This paper deals with technology patents as an example of intangibles and investigates how the ALP affects MNEs' licensing strategies and welfare in a model with a tax haven. The ALP may distort MNEs' licensing decisions, because providing a license to unrelated firms restricts MNEs' profit-shifting opportunities due to the emergence of comparable transaction. Interestingly, the termination of licensing in the presence of the ALP may worsen domestic welfare if the (potential) licensee and the MNE's subsidiary do not compete in the domestic market but may improve welfare if they compete. The results under ad valorem royalty are in distinct contrast with those under per-unit royalty.</p>\",\"PeriodicalId\":47518,\"journal\":{\"name\":\"International Tax and Public Finance\",\"volume\":\" \",\"pages\":\"1-34\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2022-12-06\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9734996/pdf/\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Tax and Public Finance\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s10797-022-09770-w\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Tax and Public Finance","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s10797-022-09770-w","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

Tax havens and cross-border licensing with transfer pricing regulation.

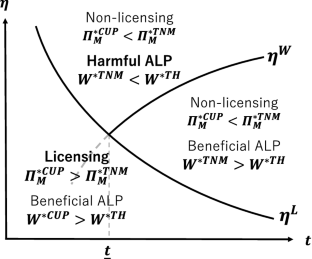

Multinational enterprises (MNEs) have incentive to reduce tax payment through transfer pricing. The incentive is stronger when MNEs own intangibles, because it is easy to transfer them across countries. To mitigate such strategic tax planning, the OECD proposes the arm's length principle (ALP). This paper deals with technology patents as an example of intangibles and investigates how the ALP affects MNEs' licensing strategies and welfare in a model with a tax haven. The ALP may distort MNEs' licensing decisions, because providing a license to unrelated firms restricts MNEs' profit-shifting opportunities due to the emergence of comparable transaction. Interestingly, the termination of licensing in the presence of the ALP may worsen domestic welfare if the (potential) licensee and the MNE's subsidiary do not compete in the domestic market but may improve welfare if they compete. The results under ad valorem royalty are in distinct contrast with those under per-unit royalty.

期刊介绍:

INTERNATIONAL TAX AND PUBLIC FINANCE publishes outstanding original research, both theoretical and empirical, in all areas of public economics. While the journal has a historical strength in open economy, international, and interjurisdictional issues, we actively encourage high-quality submissions from the breadth of public economics.The special Policy Watch section is designed to facilitate communication between the academic and public policy spheres. This section includes timely, policy-oriented discussions. The goal is to provide a two-way forum in which academic researchers gain insight into current policy priorities and policy-makers can access academic advances in a practical way. INTERNATIONAL TAX AND PUBLIC FINANCE is peer reviewed and published in one volume per year, consisting of six issues, one of which contains papers presented at the annual congress of the International Institute of Public Finance (refereed in the usual way). Officially cited as: Int Tax Public Finance

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: