社会经济危机时期用于动态组合优化的扭曲概率算子。

IF 2.3

4区 管理学

Q3 OPERATIONS RESEARCH & MANAGEMENT SCIENCE

Central European Journal of Operations Research

Pub Date : 2022-12-09

DOI:10.1007/s10100-022-00834-0

引用次数: 0

摘要

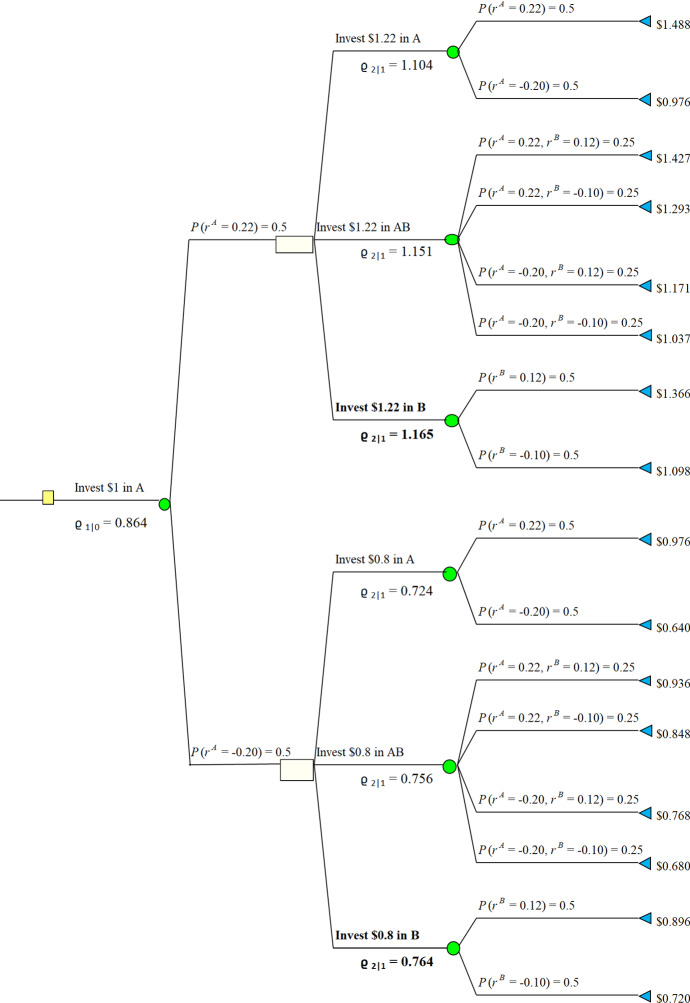

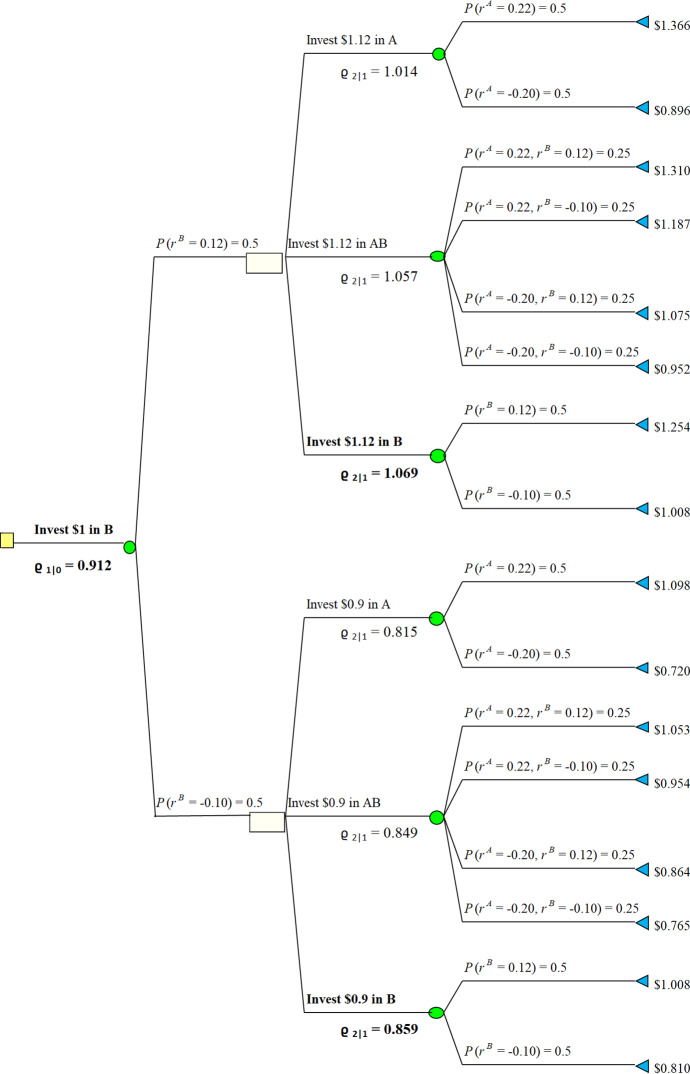

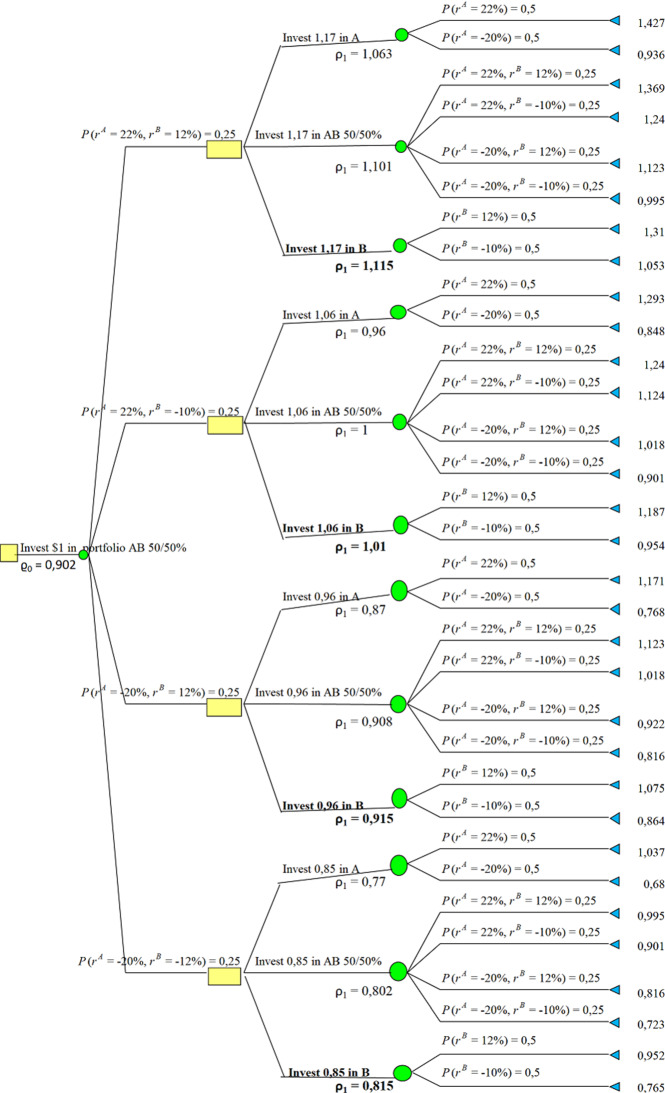

本文研究了利用概率变形对具有有限终端 T 和有界成本或财富的离散时间马尔可夫链进行稳健优化控制的问题。本文讨论了这些畸变算子的时间不一致性及其动态编程的不足。因此,引入了这些算子的动态版本,并证明了其在动态编程中的可用性。在动态编程算法的基础上,证明了最优政策的存在,并介绍了该理论在投资组合优化中的应用以及数值研究。本文章由计算机程序翻译,如有差异,请以英文原文为准。

Distorted probability operator for dynamic portfolio optimization in times of socio-economic crisis.

A robust optimal control of discrete time Markov chains with finite terminal T and bounded costs or wealth using probability distortion is studied. The time inconsistency of these distortion operators and hence its lack of dynamic programming are discussed. Due to that, dynamic versions of these operators are introduced, and its availability for dynamic programming is demonstrated. Based on dynamic programming algorithm, existence of the optimal policy is justified and an application of the theory to portfolio optimization along with a numerical study is also presented.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

Central European Journal of Operations Research

管理科学-运筹学与管理科学

CiteScore

4.70

自引率

11.80%

发文量

30

审稿时长

3 months

期刊介绍:

The Central European Journal of Operations Research provides an international readership with high quality papers that cover the theory and practice of OR and the relationship of OR methods to modern quantitative economics and business administration.

The focus is on topics such as:

- finance and banking

- measuring productivity and efficiency in the public sector

- environmental and energy issues

- computational tools for strategic decision support

- production management and logistics

- planning and scheduling

The journal publishes theoretical papers as well as application-oriented contributions and practical case studies. Occasionally, special issues feature a particular area of OR or report on the results of scientific meetings.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: