{"title":"死亡率改善率的平滑投影:贝叶斯二维样条方法。","authors":"Xiaobai Zhu, Kenneth Q Zhou","doi":"10.1007/s13385-022-00323-3","DOIUrl":null,"url":null,"abstract":"<p><p>This paper proposes a spline mortality model for generating smooth projections of mortality improvement rates. In particular, we follow the two-dimensional cubic B-spline approach developed by Currie et al. (Stat Model 4(4):279-298, 2004), and adopt the Bayesian estimation and LASSO penalty to overcome the limitations of spline models in forecasting mortality rates. The resulting Bayesian spline model not only provides measures of stochastic and parameter uncertainties, but also allows external opinions on future mortality to be consistently incorporated. The mortality improvement rates projected by the proposed model are smoothly transitioned from the historical values with short-term trends shown in recent observations to the long-term terminal rates suggested by external opinions. Our technical work is complemented by numerical illustrations that use real mortality data and external rates to showcase the features of the proposed model.</p>","PeriodicalId":44305,"journal":{"name":"European Actuarial Journal","volume":"13 1","pages":"277-305"},"PeriodicalIF":1.6000,"publicationDate":"2023-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9243738/pdf/","citationCount":"0","resultStr":"{\"title\":\"Smooth projection of mortality improvement rates: a Bayesian two-dimensional spline approach.\",\"authors\":\"Xiaobai Zhu, Kenneth Q Zhou\",\"doi\":\"10.1007/s13385-022-00323-3\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><p>This paper proposes a spline mortality model for generating smooth projections of mortality improvement rates. In particular, we follow the two-dimensional cubic B-spline approach developed by Currie et al. (Stat Model 4(4):279-298, 2004), and adopt the Bayesian estimation and LASSO penalty to overcome the limitations of spline models in forecasting mortality rates. The resulting Bayesian spline model not only provides measures of stochastic and parameter uncertainties, but also allows external opinions on future mortality to be consistently incorporated. The mortality improvement rates projected by the proposed model are smoothly transitioned from the historical values with short-term trends shown in recent observations to the long-term terminal rates suggested by external opinions. Our technical work is complemented by numerical illustrations that use real mortality data and external rates to showcase the features of the proposed model.</p>\",\"PeriodicalId\":44305,\"journal\":{\"name\":\"European Actuarial Journal\",\"volume\":\"13 1\",\"pages\":\"277-305\"},\"PeriodicalIF\":1.6000,\"publicationDate\":\"2023-01-01\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9243738/pdf/\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"European Actuarial Journal\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s13385-022-00323-3\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q4\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"European Actuarial Journal","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s13385-022-00323-3","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q4","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

摘要

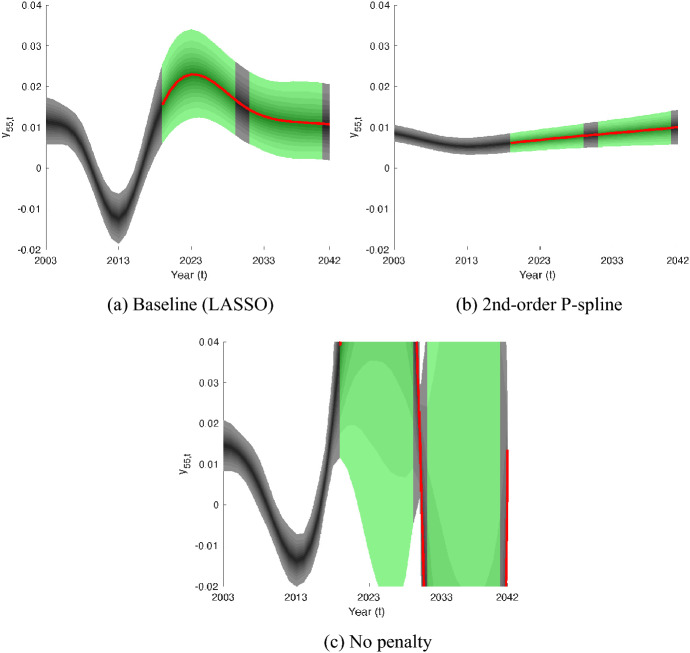

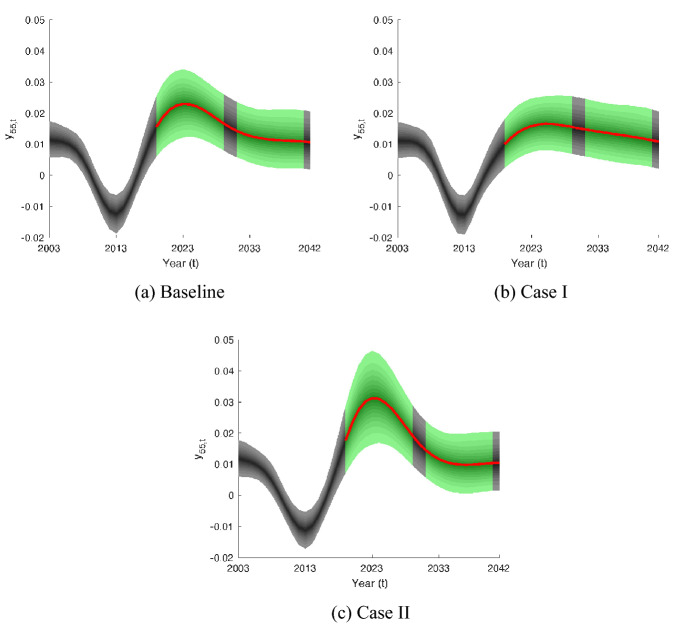

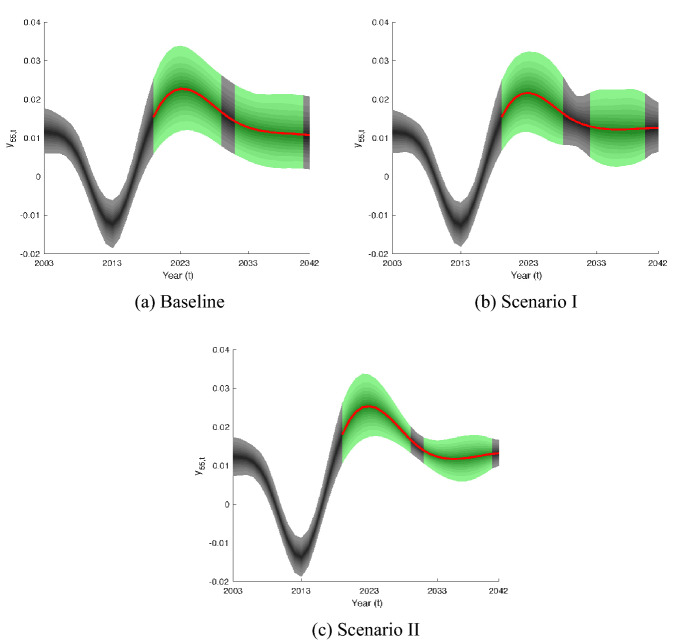

本文提出了一个样条死亡率模型,用于生成死亡率改善率的平滑预测。特别是,我们遵循Currie等人开发的二维三次b样条方法(Stat Model 4(4):279-298, 2004),并采用贝叶斯估计和LASSO惩罚来克服样条模型在预测死亡率方面的局限性。由此产生的贝叶斯样条模型不仅提供了随机和参数不确定性的度量,而且还允许对未来死亡率的外部意见一致地纳入。拟议模式预估的死亡率改善率从最近观测显示的具有短期趋势的历史值平稳地过渡到外部意见所建议的长期终端率。我们的技术工作还辅以数字插图,这些插图使用真实的死亡率数据和外部比率来展示所提出模型的特点。

Smooth projection of mortality improvement rates: a Bayesian two-dimensional spline approach.

This paper proposes a spline mortality model for generating smooth projections of mortality improvement rates. In particular, we follow the two-dimensional cubic B-spline approach developed by Currie et al. (Stat Model 4(4):279-298, 2004), and adopt the Bayesian estimation and LASSO penalty to overcome the limitations of spline models in forecasting mortality rates. The resulting Bayesian spline model not only provides measures of stochastic and parameter uncertainties, but also allows external opinions on future mortality to be consistently incorporated. The mortality improvement rates projected by the proposed model are smoothly transitioned from the historical values with short-term trends shown in recent observations to the long-term terminal rates suggested by external opinions. Our technical work is complemented by numerical illustrations that use real mortality data and external rates to showcase the features of the proposed model.

期刊介绍:

Actuarial science and actuarial finance deal with the study, modeling and managing of insurance and related financial risks for which stochastic models and statistical methods are available. Topics include classical actuarial mathematics such as life and non-life insurance, pension funds, reinsurance, and also more recent areas of interest such as risk management, asset-and-liability management, solvency, catastrophe modeling, systematic changes in risk parameters, longevity, etc. EAJ is designed for the promotion and development of actuarial science and actuarial finance. For this, we publish original actuarial research papers, either theoretical or applied, with innovative applications, as well as case studies on the evaluation and implementation of new mathematical methods in insurance and actuarial finance. We also welcome survey papers on topics of recent interest in the field. EAJ is the successor of six national actuarial journals, and particularly focuses on links between actuarial theory and practice. In order to serve as a platform for this exchange, we also welcome discussions (typically from practitioners, with a length of 1-3 pages) on published papers that highlight the application aspects of the discussed paper. Such discussions can also suggest modifications of the studied problem which are of particular interest to actuarial practice. Thus, they can serve as motivation for further studies.Finally, EAJ now also publishes ‘Letters’, which are short papers (up to 5 pages) that have academic and/or practical relevance and consist of e.g. an interesting idea, insight, clarification or observation of a cross-connection that deserves publication, but is shorter than a usual research article. A detailed description or proposition of a new relevant research question, short but curious mathematical results that deserve the attention of the actuarial community as well as novel applications of mathematical and actuarial concepts are equally welcome. Letter submissions will be reviewed within 6 weeks, so that they provide an opportunity to get good and pertinent ideas published quickly, while the same refereeing standards as for other submissions apply. Both academics and practitioners are encouraged to contribute to this new format. Authors are invited to submit their papers online via http://euaj.edmgr.com.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: