{"title":"Goods and Services Tax (GST) Implementation in India: A SAP-LAP-Twitter Analytic Perspective.","authors":"Arun Kumar Deshmukh, Ashutosh Mohan, Ishi Mohan","doi":"10.1007/s40171-021-00297-3","DOIUrl":null,"url":null,"abstract":"<p><p>In a federal structure, India's determination to much-needed fiscal reforms has been widely applauded at its face value when she relinquished her previous complex and inefficient tax regime to embrace the long-awaited Goods and Services Tax (GST). It has been a significant economic move post-independence and requires validation of facts after its introduction. The present study aims to present a general macroeconomic analysis of the extent to which the adoption of GST has improved existing tax administration and resultant general economic well-being of a democratic political economy like India in light of innovation implementation theoretical perspective. Further, the study tried to determine how the stakeholders perceived such big-bang reform even after the three years of its adoption. The study attempted to assess to what extent the adoption of GST has indeed influenced the economy in general and citizens and/or consumers in particular while using a case-based qualitative inquiry. The present research applied the situation-actor-process; learning-action-performance analysis framework for the case analysis. The facts reveal that India has observed a tremendous increase in tax base vis-à-vis revenue collection. Yet, some efforts are desired to improve the low tax to GDP ratio, skewed GST payers base, negative stakeholders' perception of GST (revealed through Twitter sentiment analysis), and the evil of tax evasion. The other merits realized by the economy are presented as benefits to the consumers, MSMEs, improved ease of doing business ranking, and foster make-in-India and <i>AatmanirbharBharat</i> move by the government.</p>","PeriodicalId":34933,"journal":{"name":"Global Journal of Flexible Systems Management","volume":"23 2","pages":"165-183"},"PeriodicalIF":0.0000,"publicationDate":"2022-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC8790948/pdf/","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Global Journal of Flexible Systems Management","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s40171-021-00297-3","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2022/1/26 0:00:00","PubModel":"Epub","JCR":"Q1","JCRName":"Business, Management and Accounting","Score":null,"Total":0}

引用次数: 0

Abstract

In a federal structure, India's determination to much-needed fiscal reforms has been widely applauded at its face value when she relinquished her previous complex and inefficient tax regime to embrace the long-awaited Goods and Services Tax (GST). It has been a significant economic move post-independence and requires validation of facts after its introduction. The present study aims to present a general macroeconomic analysis of the extent to which the adoption of GST has improved existing tax administration and resultant general economic well-being of a democratic political economy like India in light of innovation implementation theoretical perspective. Further, the study tried to determine how the stakeholders perceived such big-bang reform even after the three years of its adoption. The study attempted to assess to what extent the adoption of GST has indeed influenced the economy in general and citizens and/or consumers in particular while using a case-based qualitative inquiry. The present research applied the situation-actor-process; learning-action-performance analysis framework for the case analysis. The facts reveal that India has observed a tremendous increase in tax base vis-à-vis revenue collection. Yet, some efforts are desired to improve the low tax to GDP ratio, skewed GST payers base, negative stakeholders' perception of GST (revealed through Twitter sentiment analysis), and the evil of tax evasion. The other merits realized by the economy are presented as benefits to the consumers, MSMEs, improved ease of doing business ranking, and foster make-in-India and AatmanirbharBharat move by the government.

期刊介绍:

Aim

This journal intends to share concepts, researches and practical experiences to enable the organizations to become more flexible (adaptive, responsive, and agile) at the level of strategy, structure, systems, people, and culture. Flexibility relates to providing more options, quicker change mechanisms, and enhanced freedom of choice so as to respond to the changing situation with minimum time and efforts.

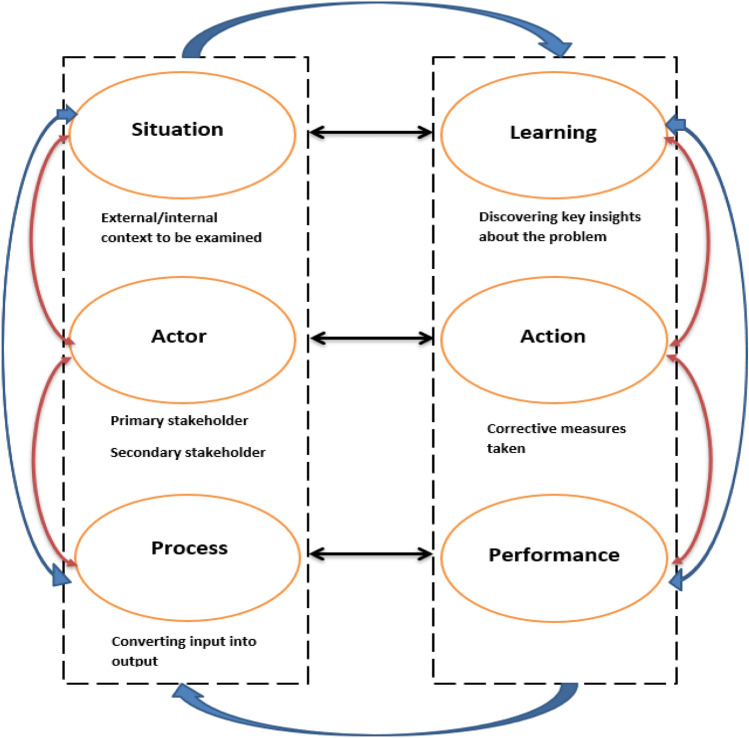

It aims to make contributions in this direction to both the world of work and the world of knowledge so as to continuously evolve and enrich the flexible systems management paradigm at a generic level as well as specifically testing and innovating the use of SAP-LAP (Situation- Actor - Process-Learning-Action-Performance) framework in varied managerial situations to cope with the challenges of the new business models and frameworks. It is a General Management Journal with a focus on flexibility.

Scope

The Journal includes papers relating to: conceptual frameworks, empirical studies, case experiences, insights, strategies, organizational frameworks, applications and systems, methodologies and models, tools and techniques, innovations, comparative practices, scenarios, and reviews.

The papers may be covering one or many of the following areas: Dimensions of enterprise flexibility, Connotations of flexibility, and Emerging managerial issues/approaches, generating and demanding flexibility.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: