{"title":"Providing pandemic business interruption coverage with double trigger cat bonds.","authors":"André Schmitt, Sandrine Spaeter","doi":"10.1057/s41288-023-00299-5","DOIUrl":null,"url":null,"abstract":"<p><p>The aim of this paper is to show how qualified investors in cat bonds can offer adequate pandemic business interruption protection in a comprehensive public-private coverage scheme. First, we propose a numerical model to expose how cat bonds can contribute to complement standard re/insurance by improving coverage of cedents even though risks are positively correlated during a pandemic. Second, we introduce double trigger pandemic business interruption cat bonds, which we name PBI bonds, and discuss their precise characteristics to provide efficient coverage. A first trigger should be pulled when the World Health Organization declares a Public Health Emergency of International Concern (PHEIC). The second trigger determines the payout of the bond based on the modelised business interruption losses of an industry in a country. We discuss moral hazard, basis risk, correlation and liquidity issues which are critical in the context of a pandemic. Third, we simulate the life of theoretical PBI bonds in the restaurant industry in France by using data gathered during the COVID-19 pandemic.</p>","PeriodicalId":75009,"journal":{"name":"The Geneva papers on risk and insurance. Issues and practice","volume":" ","pages":"1-27"},"PeriodicalIF":3.3000,"publicationDate":"2023-05-30","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10228458/pdf/","citationCount":"1","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"The Geneva papers on risk and insurance. Issues and practice","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1057/s41288-023-00299-5","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

引用次数: 1

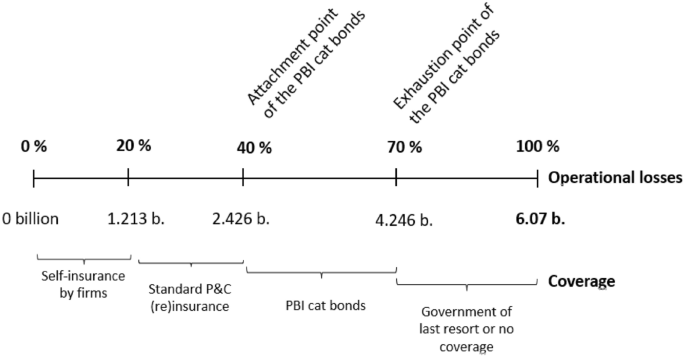

Abstract

The aim of this paper is to show how qualified investors in cat bonds can offer adequate pandemic business interruption protection in a comprehensive public-private coverage scheme. First, we propose a numerical model to expose how cat bonds can contribute to complement standard re/insurance by improving coverage of cedents even though risks are positively correlated during a pandemic. Second, we introduce double trigger pandemic business interruption cat bonds, which we name PBI bonds, and discuss their precise characteristics to provide efficient coverage. A first trigger should be pulled when the World Health Organization declares a Public Health Emergency of International Concern (PHEIC). The second trigger determines the payout of the bond based on the modelised business interruption losses of an industry in a country. We discuss moral hazard, basis risk, correlation and liquidity issues which are critical in the context of a pandemic. Third, we simulate the life of theoretical PBI bonds in the restaurant industry in France by using data gathered during the COVID-19 pandemic.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: