{"title":"A study of Fisher Effect in India.","authors":"Swapnil Suryavanshi","doi":"10.1007/s41775-023-00180-1","DOIUrl":null,"url":null,"abstract":"<p><p>In this paper, the relationship between nominal interest rate and inflation is analyzed based on Fisher Effect (FE) theory. As per FE theory, the difference between nominal interest rate and expected inflation is equal to real interest rate. The theory proposes that a rise in expected inflation can lead to positive impact on nominal interest rate when the real interest rate is constant. For analyzing FE, the inflation rate measures based on Core index, Wholesale Price Index (WPI) and Consumer Price Index (CPI) are considered. As per rational expectation hypothesis, the one-period-ahead inflation rate is considered as expected inflation (eInf). The interest rates (IR) associated with call money, treasury bills of 91- and 364-day maturities are considered. The study uses ARDL bounds testing approach and Granger causality test for analyzing the long-run relationship between eInf and IR. The study finds evidence for presence of cointegrating relationship between eInf and IR in India. Contrary to FE theory, the long-run relation between eInf and IR is found to be negative. The extent and significance of long-run relationship varies depending on measures of eInf and IR considered. Along with cointegration, the expected WPI inflation and interest rate measures also exhibit Granger causality in at least one direction. Although, the cointegration is not observed between expected CPI and IR, there exists Granger causality between these variables. This increasing disconnect between eInf and IR could be attributed to adoption of flexible inflation targeting framework, pursual of additional objectives by monetary authority, different sources and types of inflation, etc.</p>","PeriodicalId":36028,"journal":{"name":"Indian Economic Review","volume":" ","pages":"1-19"},"PeriodicalIF":0.6000,"publicationDate":"2023-05-31","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10230480/pdf/","citationCount":"1","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Indian Economic Review","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s41775-023-00180-1","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"Economics, Econometrics and Finance","Score":null,"Total":0}

引用次数: 1

Abstract

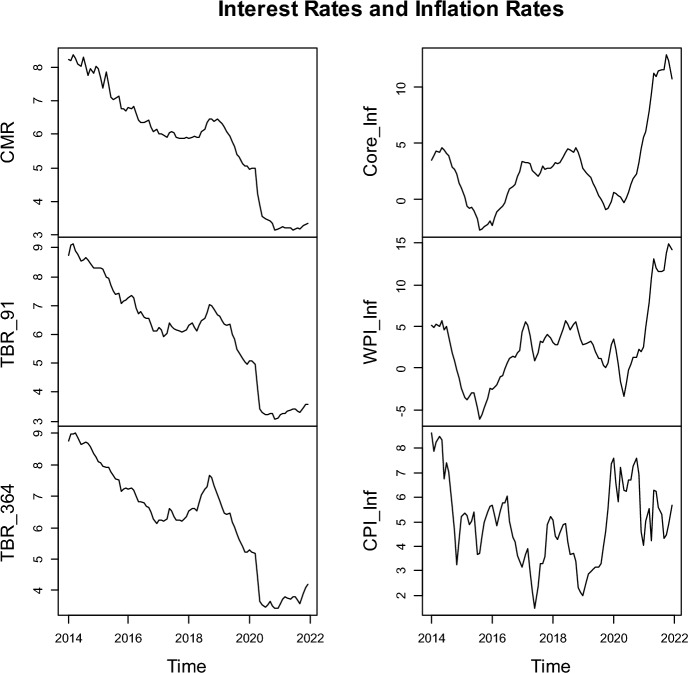

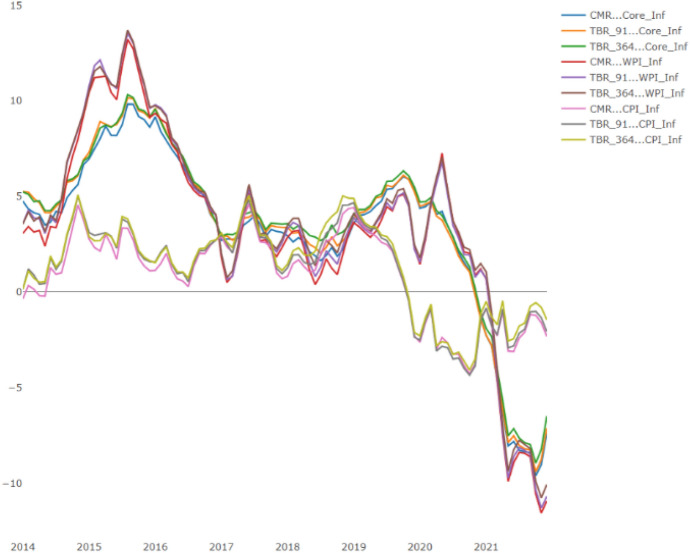

In this paper, the relationship between nominal interest rate and inflation is analyzed based on Fisher Effect (FE) theory. As per FE theory, the difference between nominal interest rate and expected inflation is equal to real interest rate. The theory proposes that a rise in expected inflation can lead to positive impact on nominal interest rate when the real interest rate is constant. For analyzing FE, the inflation rate measures based on Core index, Wholesale Price Index (WPI) and Consumer Price Index (CPI) are considered. As per rational expectation hypothesis, the one-period-ahead inflation rate is considered as expected inflation (eInf). The interest rates (IR) associated with call money, treasury bills of 91- and 364-day maturities are considered. The study uses ARDL bounds testing approach and Granger causality test for analyzing the long-run relationship between eInf and IR. The study finds evidence for presence of cointegrating relationship between eInf and IR in India. Contrary to FE theory, the long-run relation between eInf and IR is found to be negative. The extent and significance of long-run relationship varies depending on measures of eInf and IR considered. Along with cointegration, the expected WPI inflation and interest rate measures also exhibit Granger causality in at least one direction. Although, the cointegration is not observed between expected CPI and IR, there exists Granger causality between these variables. This increasing disconnect between eInf and IR could be attributed to adoption of flexible inflation targeting framework, pursual of additional objectives by monetary authority, different sources and types of inflation, etc.

Indian Economic ReviewEconomics, Econometrics and Finance-Economics, Econometrics and Finance (miscellaneous)

CiteScore

2.10

自引率

0.00%

发文量

12

期刊介绍:

The Indian Economic Review aims to provide a platform for dissemination of innovative research in economics that employs theoretical and empirical approaches. Original research in all areas of economics is welcome. These areas include but are not limited toAgricultural and resource economics Behavioural economics Development economics Economic theory Economics of health and education Environmental economics Experimental economics Game theory Industrial organisation International trade and finance Law and economics Macro and monetary economics Poverty and inequality

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: