{"title":"Stakeholder arguments during the adoption of a sugar sweetened beverage tax in South Africa and their influence: a content analysis.","authors":"Safura Abdool Karim, Petronell Kruger, Natasha Mazonde, Agnes Erzse, Susan Goldstein, Karen Hofman","doi":"10.1080/16549716.2022.2152638","DOIUrl":null,"url":null,"abstract":"<p><strong>Background: </strong>Sugar-sweetened beverage (SSB) taxes are recognised as an effective intervention to prevent obesity. More countries are adopting SSB taxes, but the process of the adoption is politically complex.</p><p><strong>Objective: </strong>This study aimed to analyse how public participation processes influenced the South African tax.</p><p><strong>Methods: </strong>We conducted a content analysis of documents associated with the process of adopting the tax. Records were identified utilising the Parliamentary Monitoring Group database, including draft bills, meeting minutes and written submissions. The records were categorised and then inductively coded to identify themes and arguments.</p><p><strong>Results: </strong>We identified six cross-cutting themes advanced by stakeholders: economic considerations, impact on the vulnerable, responsiveness of an SSB tax to the problem of obesity, appropriateness of an SSB tax in South Africa, procedural concerns, and structure of the tax. Stakeholder views and arguments about the tax diverged based on their vested interests. The primary policymaker was most responsive to arguments concerning the economic impact of a tax, procedural concerns and the structure of the tax, reducing the effective rate to address industry concerns.</p><p><strong>Conclusion: </strong>Both supportive and opposing stakeholders influenced the tax. Economic arguments had a significant impact. Arguments in South Africa broadly echoed arguments advanced in many other jurisdictions.</p>","PeriodicalId":49197,"journal":{"name":"Global Health Action","volume":"16 1","pages":"2152638"},"PeriodicalIF":2.6000,"publicationDate":"2023-12-31","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9754008/pdf/","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Global Health Action","FirstCategoryId":"3","ListUrlMain":"https://doi.org/10.1080/16549716.2022.2152638","RegionNum":3,"RegionCategory":"医学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"PUBLIC, ENVIRONMENTAL & OCCUPATIONAL HEALTH","Score":null,"Total":0}

引用次数: 0

Abstract

Background: Sugar-sweetened beverage (SSB) taxes are recognised as an effective intervention to prevent obesity. More countries are adopting SSB taxes, but the process of the adoption is politically complex.

Objective: This study aimed to analyse how public participation processes influenced the South African tax.

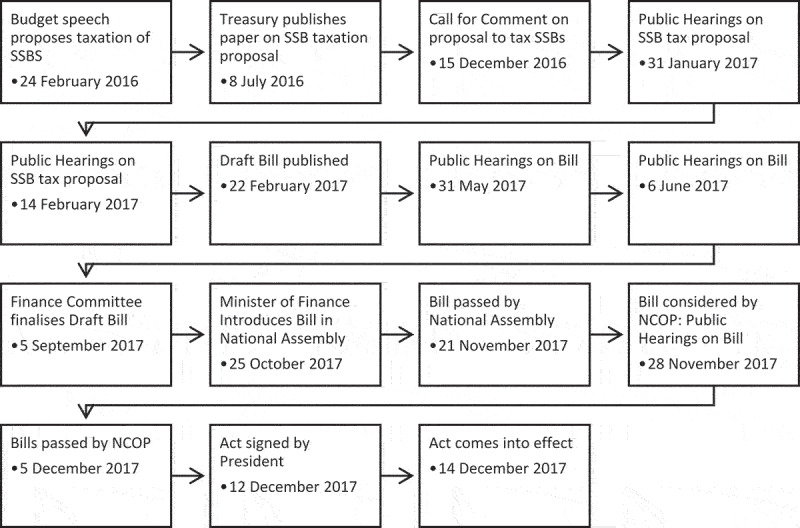

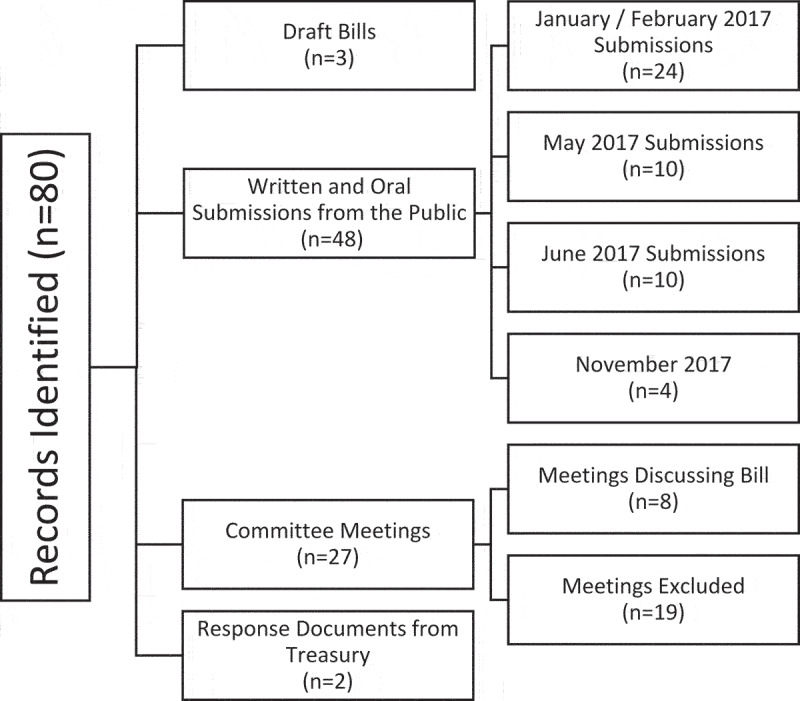

Methods: We conducted a content analysis of documents associated with the process of adopting the tax. Records were identified utilising the Parliamentary Monitoring Group database, including draft bills, meeting minutes and written submissions. The records were categorised and then inductively coded to identify themes and arguments.

Results: We identified six cross-cutting themes advanced by stakeholders: economic considerations, impact on the vulnerable, responsiveness of an SSB tax to the problem of obesity, appropriateness of an SSB tax in South Africa, procedural concerns, and structure of the tax. Stakeholder views and arguments about the tax diverged based on their vested interests. The primary policymaker was most responsive to arguments concerning the economic impact of a tax, procedural concerns and the structure of the tax, reducing the effective rate to address industry concerns.

Conclusion: Both supportive and opposing stakeholders influenced the tax. Economic arguments had a significant impact. Arguments in South Africa broadly echoed arguments advanced in many other jurisdictions.

期刊介绍:

Global Health Action is an international peer-reviewed Open Access journal affiliated with the Unit of Epidemiology and Global Health, Department of Public Health and Clinical Medicine at Umeå University, Sweden. The Unit hosts the Umeå International School of Public Health and the Umeå Centre for Global Health Research.

Vision: Our vision is to be a leading journal in the global health field, narrowing health information gaps and contributing to the implementation of policies and actions that lead to improved global health.

Aim: The widening gap between the winners and losers of globalisation presents major public health challenges. To meet these challenges, it is crucial to generate new knowledge and evidence in the field and in settings where the evidence is lacking, as well as to bridge the gaps between existing knowledge and implementation of relevant findings. Thus, the aim of Global Health Action is to contribute to fuelling a more concrete, hands-on approach to addressing global health challenges. Manuscripts suggesting strategies for practical interventions and research implementations where none already exist are specifically welcomed. Further, the journal encourages articles from low- and middle-income countries, while also welcoming articles originated from South-South and South-North collaborations. All articles are expected to address a global agenda and include a strong implementation or policy component.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: