José E. Figueroa-López, Hyoeun Lee, Raghu Pasupathy

{"title":"Optimal placement of a small order in a diffusive limit order book","authors":"José E. Figueroa-López, Hyoeun Lee, Raghu Pasupathy","doi":"10.1002/hf2.10017","DOIUrl":null,"url":null,"abstract":"<p>We study the optimal placement problem of a stock trader who wishes to clear his/her inventory by a predetermined time horizon <i>t</i>, using a limit order or a market order. For a diffusive market, we characterize the optimal limit order placement policy and analyze its behavior under different market conditions. In particular, we show that, in the presence of a negative drift, there exists a critical time <i>t</i><sub>0</sub> > 0 such that, for any time horizon <i>t</i> > <i>t</i><sub>0</sub>, there exists an optimal placement, which, contrary to earlier work, is different from one that is placed “infinitesimally” close to the best ask, such as the best bid and second best bid. We also propose a simple method to approximate the critical time <i>t</i><sub>0</sub> and the optimal order placement.</p>","PeriodicalId":100604,"journal":{"name":"High Frequency","volume":"1 2","pages":"87-116"},"PeriodicalIF":0.0000,"publicationDate":"2018-04-06","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://sci-hub-pdf.com/10.1002/hf2.10017","citationCount":"1","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"High Frequency","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/hf2.10017","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

引用次数: 1

Abstract

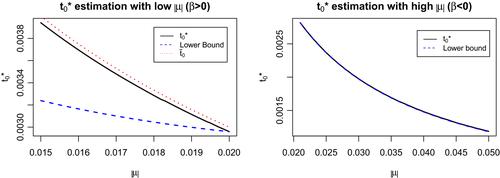

We study the optimal placement problem of a stock trader who wishes to clear his/her inventory by a predetermined time horizon t, using a limit order or a market order. For a diffusive market, we characterize the optimal limit order placement policy and analyze its behavior under different market conditions. In particular, we show that, in the presence of a negative drift, there exists a critical time t0 > 0 such that, for any time horizon t > t0, there exists an optimal placement, which, contrary to earlier work, is different from one that is placed “infinitesimally” close to the best ask, such as the best bid and second best bid. We also propose a simple method to approximate the critical time t0 and the optimal order placement.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: