Jenny Hatchard, Penny Buykx, Alan Brennan, Duncan Gillespie

{"title":"Options for modifying UK alcohol and tobacco tax: A rapid scoping review of the evidence over the period 1997-2018.","authors":"Jenny Hatchard, Penny Buykx, Alan Brennan, Duncan Gillespie","doi":"10.3310/nihropenres.13379.2","DOIUrl":null,"url":null,"abstract":"<p><strong>Background: </strong>Increased taxation is recognised worldwide as one of the most effective interventions for decreasing tobacco and harmful alcohol use, with many variations of policy options available. This rapid scoping review was part of a NIHR-funded project ('SYNTAX' 16/105/26) and was undertaken during 2018 to inform interviews to be conducted with UK public health stakeholders with expertise in alcohol and tobacco pricing policy.</p><p><strong>Methods: </strong>Objectives: To synthesise evidence and debates on current and potential alcohol and tobacco taxation options for the UK, and report on the underlying objectives, evidence of effects and mediating factors. Eligibility criteria: Peer-reviewed and grey literature; published 1997-2018; English language; UK-focused; include taxation interventions for alcohol, tobacco, or both. Sources of evidence: PubMed, Scopus, Cochrane Library, Google, stakeholder and colleague recommendations.</p><p><strong>Charting methods: </strong>Excel spreadsheet structured using PICO framework, recording source characteristics and content.</p><p><strong>Results: </strong>Ninety-one sources qualified for inclusion: 49 alcohol, 36 tobacco, 6 both. Analysis identified four policy themes: changes to excise duty within existing tax structures, structural reforms, industry measures, and hypothecation of tax revenue for public benefits. For alcohol, policy options focused on raising the price of cheap, high-strength alcohol. For tobacco, policy options focused on raising the price of all tobacco products, especially the cheapest products, which are hand-rolling tobacco. For alcohol and tobacco, there were options such as levies that take money from the industries to help reduce the societal costs of their products. Due to the perceived social and economic importance of alcohol in contrast to tobacco, policy options also discussed supporting pubs and small breweries.</p><p><strong>Conclusions: </strong>This review has identified a set of tax policy options for tobacco and alcohol, their objectives, evidence of effects and related mediating factors. The differences between alcohol and tobacco tax policy options and debates suggest an opportunity for cross-substance policy learning.</p>","PeriodicalId":74312,"journal":{"name":"NIHR open research","volume":"3 ","pages":"26"},"PeriodicalIF":0.0000,"publicationDate":"2023-10-30","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10593339/pdf/","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"NIHR open research","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.3310/nihropenres.13379.2","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2023/1/1 0:00:00","PubModel":"eCollection","JCR":"","JCRName":"","Score":null,"Total":0}

引用次数: 0

Abstract

Background: Increased taxation is recognised worldwide as one of the most effective interventions for decreasing tobacco and harmful alcohol use, with many variations of policy options available. This rapid scoping review was part of a NIHR-funded project ('SYNTAX' 16/105/26) and was undertaken during 2018 to inform interviews to be conducted with UK public health stakeholders with expertise in alcohol and tobacco pricing policy.

Methods: Objectives: To synthesise evidence and debates on current and potential alcohol and tobacco taxation options for the UK, and report on the underlying objectives, evidence of effects and mediating factors. Eligibility criteria: Peer-reviewed and grey literature; published 1997-2018; English language; UK-focused; include taxation interventions for alcohol, tobacco, or both. Sources of evidence: PubMed, Scopus, Cochrane Library, Google, stakeholder and colleague recommendations.

Charting methods: Excel spreadsheet structured using PICO framework, recording source characteristics and content.

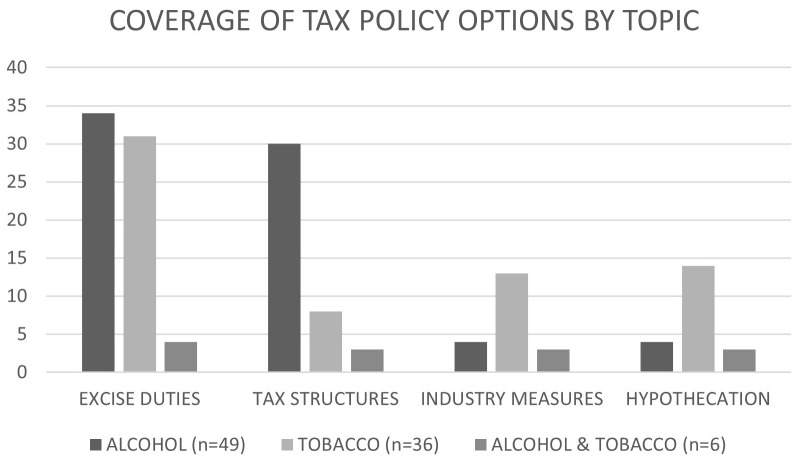

Results: Ninety-one sources qualified for inclusion: 49 alcohol, 36 tobacco, 6 both. Analysis identified four policy themes: changes to excise duty within existing tax structures, structural reforms, industry measures, and hypothecation of tax revenue for public benefits. For alcohol, policy options focused on raising the price of cheap, high-strength alcohol. For tobacco, policy options focused on raising the price of all tobacco products, especially the cheapest products, which are hand-rolling tobacco. For alcohol and tobacco, there were options such as levies that take money from the industries to help reduce the societal costs of their products. Due to the perceived social and economic importance of alcohol in contrast to tobacco, policy options also discussed supporting pubs and small breweries.

Conclusions: This review has identified a set of tax policy options for tobacco and alcohol, their objectives, evidence of effects and related mediating factors. The differences between alcohol and tobacco tax policy options and debates suggest an opportunity for cross-substance policy learning.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: