{"title":"Using Google Trends to track the global interest in International Financial Reporting Standards: Evidence from big data","authors":"Yuqian Zhang","doi":"10.1002/isaf.1529","DOIUrl":null,"url":null,"abstract":"<p>This study proposes a novel method for identifying international accounting differences under International Financial Reporting Standards (IFRS). Using Google Trends data extracted between January 2014 and August 2022, it creates an index, the Global IFRS/IAS Search Index (GISI), which comprises the search activities of 121 jurisdictions for 45 IFRS accounting standards. To assess its relative validity, I classify Nobes' (1983) 14 jurisdictions in addition to 20 OECD countries. The cluster analysis demonstrates that the GISI is a viable alternative for analyzing international differences under IFRS. The results indicate that incorporating big data could be beneficial for examining global accounting issues.</p><p>A judgmental international classification of financial reporting practices</p>","PeriodicalId":53473,"journal":{"name":"Intelligent Systems in Accounting, Finance and Management","volume":"30 2","pages":"87-100"},"PeriodicalIF":0.0000,"publicationDate":"2023-02-11","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/isaf.1529","citationCount":"1","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Intelligent Systems in Accounting, Finance and Management","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/isaf.1529","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"Economics, Econometrics and Finance","Score":null,"Total":0}

引用次数: 1

Abstract

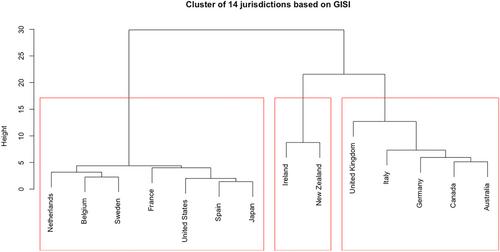

This study proposes a novel method for identifying international accounting differences under International Financial Reporting Standards (IFRS). Using Google Trends data extracted between January 2014 and August 2022, it creates an index, the Global IFRS/IAS Search Index (GISI), which comprises the search activities of 121 jurisdictions for 45 IFRS accounting standards. To assess its relative validity, I classify Nobes' (1983) 14 jurisdictions in addition to 20 OECD countries. The cluster analysis demonstrates that the GISI is a viable alternative for analyzing international differences under IFRS. The results indicate that incorporating big data could be beneficial for examining global accounting issues.

A judgmental international classification of financial reporting practices

期刊介绍:

Intelligent Systems in Accounting, Finance and Management is a quarterly international journal which publishes original, high quality material dealing with all aspects of intelligent systems as they relate to the fields of accounting, economics, finance, marketing and management. In addition, the journal also is concerned with related emerging technologies, including big data, business intelligence, social media and other technologies. It encourages the development of novel technologies, and the embedding of new and existing technologies into applications of real, practical value. Therefore, implementation issues are of as much concern as development issues. The journal is designed to appeal to academics in the intelligent systems, emerging technologies and business fields, as well as to advanced practitioners who wish to improve the effectiveness, efficiency, or economy of their working practices. A special feature of the journal is the use of two groups of reviewers, those who specialize in intelligent systems work, and also those who specialize in applications areas. Reviewers are asked to address issues of originality and actual or potential impact on research, teaching, or practice in the accounting, finance, or management fields. Authors working on conceptual developments or on laboratory-based explorations of data sets therefore need to address the issue of potential impact at some level in submissions to the journal.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: