David Lindermüller, Irina Lindermüller, Christian Nitzl, Bernhard Hirsch

{"title":"Antecedents of public-sector auditors’ economic error communication: Evidence from Germany","authors":"David Lindermüller, Irina Lindermüller, Christian Nitzl, Bernhard Hirsch","doi":"10.1111/faam.12364","DOIUrl":null,"url":null,"abstract":"<p>Traditionally, public-sector auditors are concerned with auditing the legality and regularity of government activities (compliance audits). However, such auditors are increasingly expected to conduct “performance audits” and communicate economic errors due to inefficiency, ineffectiveness, and poor economic decisions to the auditee. This type of role change is often accompanied by role stress. This study explores whether role stress—role conflict and role ambiguity—among local public-sector auditors and their perception of their new business partner role are precursors of their communication of detected economic errors to their auditees. Therefore, survey data from German local public sector auditors (i.e., municipalities and counties) are gathered and analyzed. Our results show that compare to those in other organizations, auditors who work in more formalized public-sector audit organizations are less likely to experience role ambiguity and role conflict and to communicate auditees’ economic errors more actively. Furthermore, we find that auditors who do not experience role ambiguity find it easier to see themselves as a business partner of the auditee and show more active economic error communication. The present study informs the literature on performance auditing by transferring the business partner concept to the context of public-sector auditing and applying a role theory perspective to reveal drivers of economic error communication.</p>","PeriodicalId":47120,"journal":{"name":"Financial Accountability & Management","volume":"39 3","pages":"593-615"},"PeriodicalIF":2.6000,"publicationDate":"2023-04-04","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/faam.12364","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Financial Accountability & Management","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/faam.12364","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

Abstract

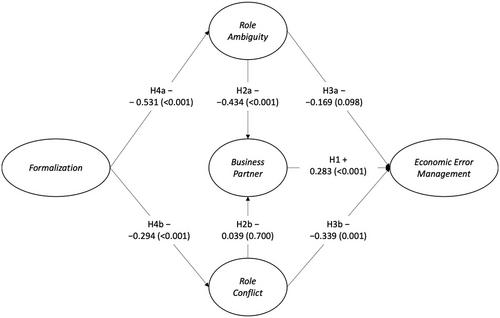

Traditionally, public-sector auditors are concerned with auditing the legality and regularity of government activities (compliance audits). However, such auditors are increasingly expected to conduct “performance audits” and communicate economic errors due to inefficiency, ineffectiveness, and poor economic decisions to the auditee. This type of role change is often accompanied by role stress. This study explores whether role stress—role conflict and role ambiguity—among local public-sector auditors and their perception of their new business partner role are precursors of their communication of detected economic errors to their auditees. Therefore, survey data from German local public sector auditors (i.e., municipalities and counties) are gathered and analyzed. Our results show that compare to those in other organizations, auditors who work in more formalized public-sector audit organizations are less likely to experience role ambiguity and role conflict and to communicate auditees’ economic errors more actively. Furthermore, we find that auditors who do not experience role ambiguity find it easier to see themselves as a business partner of the auditee and show more active economic error communication. The present study informs the literature on performance auditing by transferring the business partner concept to the context of public-sector auditing and applying a role theory perspective to reveal drivers of economic error communication.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: