Dinesh Ramdhony, Francisco Liébana-Cabanillas, Vidisha Devi Gunesh-Ramlugun, Fariha Mowlabocus

{"title":"Modelling the determinants of electronic tax filing services’ continuance usage intention","authors":"Dinesh Ramdhony, Francisco Liébana-Cabanillas, Vidisha Devi Gunesh-Ramlugun, Fariha Mowlabocus","doi":"10.1111/1467-8500.12559","DOIUrl":null,"url":null,"abstract":"<p>The success of electronic filing services largely depends on their continuance usage. This study examines the factors affecting the continuance usage intention of the online tax filing services in Mauritius. An integrated model comprising Trust Theory and Information System Success Model (ISSM) is applied to assess the continuance usage behaviour of e-filing systems. The model has been extended by adding two additional variables: Perceived Usefulness and Perceived Risk. The model was tested using a sample of 315 users of e-filing services in Mauritius. A structural equation modelling technique using partial least square structural equation modelling verified the hypotheses. The results reveal that the continuance usage intention of an electronic tax filing system is influenced by Perceived Usefulness, User Satisfaction, and Service Quality. However, Perceived Risk does not influence the continuance usage intention of e-filing systems since the importance of Perceived Risk diminishes as trust in the e-service provider increases. The theoretical and practical implications derived from the findings of this study are also discussed. This paper makes several contributions to the literature on electronic tax filing systems.</p>","PeriodicalId":47373,"journal":{"name":"Australian Journal of Public Administration","volume":"82 2","pages":"194-209"},"PeriodicalIF":2.1000,"publicationDate":"2022-10-13","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1467-8500.12559","citationCount":"1","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Australian Journal of Public Administration","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1467-8500.12559","RegionNum":4,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"PUBLIC ADMINISTRATION","Score":null,"Total":0}

引用次数: 1

Abstract

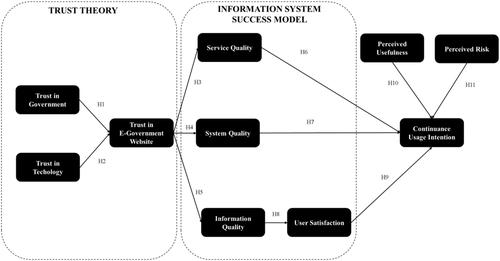

The success of electronic filing services largely depends on their continuance usage. This study examines the factors affecting the continuance usage intention of the online tax filing services in Mauritius. An integrated model comprising Trust Theory and Information System Success Model (ISSM) is applied to assess the continuance usage behaviour of e-filing systems. The model has been extended by adding two additional variables: Perceived Usefulness and Perceived Risk. The model was tested using a sample of 315 users of e-filing services in Mauritius. A structural equation modelling technique using partial least square structural equation modelling verified the hypotheses. The results reveal that the continuance usage intention of an electronic tax filing system is influenced by Perceived Usefulness, User Satisfaction, and Service Quality. However, Perceived Risk does not influence the continuance usage intention of e-filing systems since the importance of Perceived Risk diminishes as trust in the e-service provider increases. The theoretical and practical implications derived from the findings of this study are also discussed. This paper makes several contributions to the literature on electronic tax filing systems.

期刊介绍:

Aimed at a diverse readership, the Australian Journal of Public Administration is committed to the study and practice of public administration, public management and policy making. It encourages research, reflection and commentary amongst those interested in a range of public sector settings - federal, state, local and inter-governmental. The journal focuses on Australian concerns, but welcomes manuscripts relating to international developments of relevance to Australian experience.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: