Media Coverage, Real Earnings Management, and Long-Run Market Performance: Evidence from Chinese IPOs

Abstract

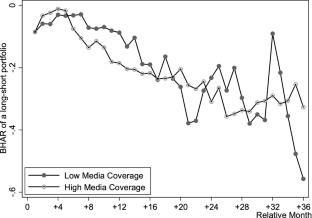

This study investigates how real earnings management (REM) in the initial public offering (IPO) year affects long-run post-IPO market performance. The empirical results show that the effect of REM on a firm’s stock returns varies with the forms of REM. Abnormal production costs are positively associated with long-run returns, whereas abnormal cuts in discretionary expenses are negatively associated with long-run returns. These results suggest that investors are not fully aware of the implications of REM and initially undervalue or overvalue the firm based on different REM activities. Further, this study examines the long-run role of the media in the capital market by examining the impact of media coverage on the consequences of IPO firms’ REM practices. The results indicate that the associations between REM and stock returns become weaker if the IPO firm is more visible through the media. Additional analyses show that retail investors are more likely to initially misprice REM activities and be influenced by media information. Compared with media coverage, audit quality or analyst following has a relatively less pronounced effect on the consequences of REM activities. These findings imply that media coverage appears to mitigate the influence of REM on stock returns, facilitating market efficiency after a firm’s IPO in the long run.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: