Maria Nareklishvili, Nicholas Polson, Vadim Sokolov

{"title":"Deep partial least squares for instrumental variable regression","authors":"Maria Nareklishvili, Nicholas Polson, Vadim Sokolov","doi":"10.1002/asmb.2787","DOIUrl":null,"url":null,"abstract":"<p>In this paper, we propose deep partial least squares for the estimation of high-dimensional nonlinear instrumental variable regression. As a precursor to a flexible deep neural network architecture, our methodology uses partial least squares for dimension reduction and feature selection from the set of instruments and covariates. A central theoretical result, due to Brillinger (2012) Selected Works of Daving Brillinger. 589-606, shows that the feature selection provided by partial least squares is consistent and the weights are estimated up to a proportionality constant. We illustrate our methodology with synthetic datasets with a sparse and correlated network structure and draw applications to the effect of childbearing on the mother's labor supply based on classic data of Chernozhukov et al. Ann Rev Econ. (2015b):649–688. The results on synthetic data as well as applications show that the deep partial least squares method significantly outperforms other related methods. Finally, we conclude with directions for future research.</p>","PeriodicalId":55495,"journal":{"name":"Applied Stochastic Models in Business and Industry","volume":null,"pages":null},"PeriodicalIF":1.3000,"publicationDate":"2023-06-19","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/asmb.2787","citationCount":"1","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Applied Stochastic Models in Business and Industry","FirstCategoryId":"100","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/asmb.2787","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS","Score":null,"Total":0}

引用次数: 1

Abstract

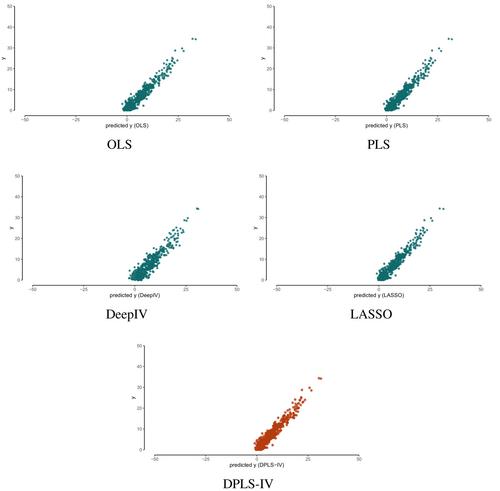

In this paper, we propose deep partial least squares for the estimation of high-dimensional nonlinear instrumental variable regression. As a precursor to a flexible deep neural network architecture, our methodology uses partial least squares for dimension reduction and feature selection from the set of instruments and covariates. A central theoretical result, due to Brillinger (2012) Selected Works of Daving Brillinger. 589-606, shows that the feature selection provided by partial least squares is consistent and the weights are estimated up to a proportionality constant. We illustrate our methodology with synthetic datasets with a sparse and correlated network structure and draw applications to the effect of childbearing on the mother's labor supply based on classic data of Chernozhukov et al. Ann Rev Econ. (2015b):649–688. The results on synthetic data as well as applications show that the deep partial least squares method significantly outperforms other related methods. Finally, we conclude with directions for future research.

期刊介绍:

ASMBI - Applied Stochastic Models in Business and Industry (formerly Applied Stochastic Models and Data Analysis) was first published in 1985, publishing contributions in the interface between stochastic modelling, data analysis and their applications in business, finance, insurance, management and production. In 2007 ASMBI became the official journal of the International Society for Business and Industrial Statistics (www.isbis.org). The main objective is to publish papers, both technical and practical, presenting new results which solve real-life problems or have great potential in doing so. Mathematical rigour, innovative stochastic modelling and sound applications are the key ingredients of papers to be published, after a very selective review process.

The journal is very open to new ideas, like Data Science and Big Data stemming from problems in business and industry or uncertainty quantification in engineering, as well as more traditional ones, like reliability, quality control, design of experiments, managerial processes, supply chains and inventories, insurance, econometrics, financial modelling (provided the papers are related to real problems). The journal is interested also in papers addressing the effects of business and industrial decisions on the environment, healthcare, social life. State-of-the art computational methods are very welcome as well, when combined with sound applications and innovative models.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: