Investment Performance and Tracking Efficiency of Indian Equity Exchange Traded Funds

Abstract

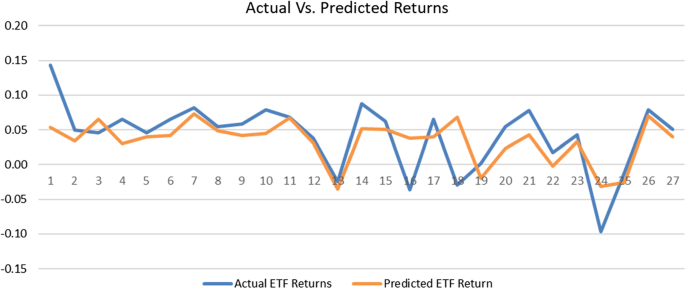

Exchange Traded Funds (ETF’s) are one of the beloved passively managed funds that offer both retail and institutional investors an access to highly profitable and wide- range of diversifiable financial assets. The study aims to assess the ability of Indian equity ETF’s in replicating the performance of their benchmark indices using a sample of 27 equity ETF’s traded on the National Stock Exchange of India during the pre-pandemic period from 01/01/2015 to 31/12/2019. Evaluation of the performance of sample ETF’s through risk-return analysis, risk-adjusted performance measures, tracking error analysis and multi-factor regression have revealed that the majority of the sample ETF’s outperformed their tracking indices but with notable tracking errors during the study period. Further, the study also indicates that the returns of the sample ETF’s have a significant and positive relationship with the returns of the index but are inversely related to risk and management fees. The results of this study will have major implications for investors in evaluating the performance of ETF’s and fund managers as well in taking suitable measures to reduce tracking errors that will help in successful replication of the benchmark along with undertaking initiatives that will enable the ETF’s to become price efficient.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: