{"title":"Arbitrage-free smile construction on FX option markets using Garman-Kohlhagen deltas and implied volatilities.","authors":"Matthias Muck","doi":"10.1007/s11147-022-09189-9","DOIUrl":null,"url":null,"abstract":"<p><p>This paper addresses arbitrage-free FX smile construction from near-term implied volatility dynamics proposed by Carr (J Financ Econ, 120(1), 1-20, 2016). The approach is directly applicable to FX option market conventions. Prices of market benchmark contracts (risk reversals and butterflies) are identified as the roots of a cubic polynomial and ATM-volatility can be matched by construction. Implied volatilities are computed with respect to (non-premium adjusted) option deltas. The approach is compared to the Vanna Volga Approach, which does not guarantee arbitrage-free prices. An empirical application to a normal and a stress scenario demonstrates that arbitrage-free implied volatilities coincide with those from the Vanna Volga Approach when prices are interpolated between the <math><mi>Δ</mi></math> 25-call and <math><mi>Δ</mi></math> 25-put options. Differences are observed when implied volatilities are extrapolated to the wings. Empirically, these differences are particularly relevant in a stress scenario during the Coronavirus crises (2020).</p>","PeriodicalId":45022,"journal":{"name":"Review of Derivatives Research","volume":"25 1","pages":"293-314"},"PeriodicalIF":0.9000,"publicationDate":"2022-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9483449/pdf/","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Review of Derivatives Research","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s11147-022-09189-9","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2022/9/18 0:00:00","PubModel":"Epub","JCR":"Q4","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

Abstract

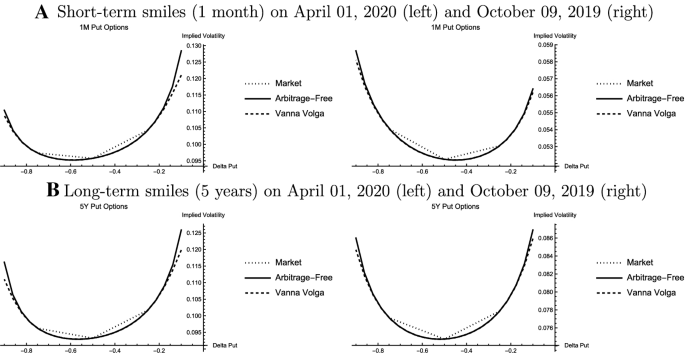

This paper addresses arbitrage-free FX smile construction from near-term implied volatility dynamics proposed by Carr (J Financ Econ, 120(1), 1-20, 2016). The approach is directly applicable to FX option market conventions. Prices of market benchmark contracts (risk reversals and butterflies) are identified as the roots of a cubic polynomial and ATM-volatility can be matched by construction. Implied volatilities are computed with respect to (non-premium adjusted) option deltas. The approach is compared to the Vanna Volga Approach, which does not guarantee arbitrage-free prices. An empirical application to a normal and a stress scenario demonstrates that arbitrage-free implied volatilities coincide with those from the Vanna Volga Approach when prices are interpolated between the 25-call and 25-put options. Differences are observed when implied volatilities are extrapolated to the wings. Empirically, these differences are particularly relevant in a stress scenario during the Coronavirus crises (2020).

期刊介绍:

The proliferation of derivative assets during the past two decades is unprecedented. With this growth in derivatives comes the need for financial institutions, institutional investors, and corporations to use sophisticated quantitative techniques to take full advantage of the spectrum of these new financial instruments. Academic research has significantly contributed to our understanding of derivative assets and markets. The growth of derivative asset markets has been accompanied by a commensurate growth in the volume of scientific research. The Review of Derivatives Research provides an international forum for researchers involved in the general areas of derivative assets. The Review publishes high-quality articles dealing with the pricing and hedging of derivative assets on any underlying asset (commodity, interest rate, currency, equity, real estate, traded or non-traded, etc.). Specific topics include but are not limited to: econometric analyses of derivative markets (efficiency, anomalies, performance, etc.) analysis of swap markets market microstructure and volatility issues regulatory and taxation issues credit risk new areas of applications such as corporate finance (capital budgeting, debt innovations), international trade (tariffs and quotas), banking and insurance (embedded options, asset-liability management) risk-sharing issues and the design of optimal derivative securities risk management, management and control valuation and analysis of the options embedded in capital projects valuation and hedging of exotic options new areas for further development (i.e. natural resources, environmental economics. The Review has a double-blind refereeing process. In contrast to the delays in the decision making and publication processes of many current journals, the Review will provide authors with an initial decision within nine weeks of receipt of the manuscript and a goal of publication within six months after acceptance. Finally, a section of the journal is available for rapid publication on `hot'' issues in the market, small technical pieces, and timely essays related to pending legislation and policy. Officially cited as: Rev Deriv Res

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: