Impact of CLERP 9 Reforms: A Longitudinal Analysis

IF 3.3

3区 管理学

Q2 BUSINESS, FINANCE

引用次数: 1

Abstract

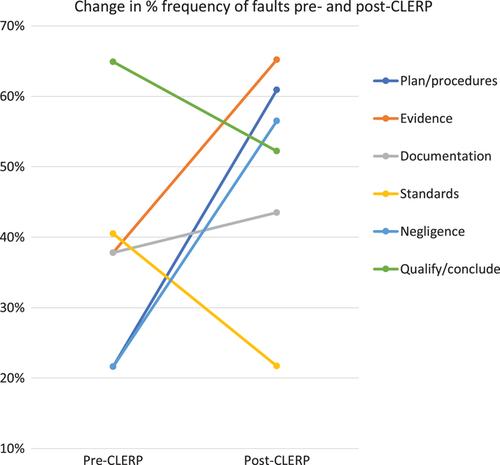

Rounds of corporate collapse linked to failure of transparency in reporting frequently result in governance reforms aimed at audit processes. The 2004 CLERP 9 reforms in Australia were intended to improve standards of auditor independence and thereby enhance auditing practice in general. This study longitudinally examines three sources of archival evidence in an Australian context, before and after the introduction of the CLERP 9 reforms. It finds little support for any success of the CLERP 9 reforms with respect to auditor independence and questions whether lack of auditor independence is in fact a significant causation factor in audit failure.

CLERP 9改革的影响:一项纵向分析

由于报告缺乏透明度而导致的几轮企业倒闭,往往导致针对审计程序的治理改革。2004年澳大利亚的CLERP 9改革旨在提高审计师独立性的标准,从而从总体上加强审计实践。本研究纵向考察了三个来源的档案证据在澳大利亚的背景下,前后引进CLERP 9改革。它发现很少有人支持CLERP 9改革在审计师独立性方面取得任何成功,并质疑缺乏审计师独立性是否实际上是审计失败的一个重要原因。

本文章由计算机程序翻译,如有差异,请以英文原文为准。

求助全文

约1分钟内获得全文

求助全文

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: