{"title":"An ISM and MICMAC Approach for Modelling the Contributors of Multibagger Stocks","authors":"Ajay Chauhan, Swati Gupta, Sanjay Gupta","doi":"10.1007/s10690-022-09394-4","DOIUrl":null,"url":null,"abstract":"<div><p>The purpose of this study is to explore the factors affecting the selection of multibagger stocks in the securities market. Further, the study aims to develop a model using interpretive structural modeling (ISM). Thereafter, the driving and dependence power of factors was found using matriced impact croises multiplication appliquee a un classement (MICMAC). A group of financial analysts and academic experts having experience in dealing in the Indian securities market were consulted and interpretive structural modelling (ISM) is adopted to develop the contextual relationship among various factors for each dimension of multibagger stocks selection. Further, to identify the driving and the dependence power of factors, the results of the ISM are used as an input to MICMAC analysis. The results of the study indicate the large potential market (C11), visionary leader (C13), unique business model (C6), understanding of the sector (C1), and promoter and management capability (C2) are the dominant factors. MICMAC analysis indicates that driving, dependent and linkage factors are 4, 5, and 4 respectively. The factors obtained for ISM model development and MICMAC analysis are based on the experts’ opinions. As it is a subjective judgment, there are chances of biasness on basis of personal opinions. A questionnaire survey can be conducted to gather viewpoints on these factors from more financial experts and portfolio consultants. The study has been executed in discussion with financial analysts and academic experts having experience in dealing in the securities market. Hence, derived results have practical validity. The securities market is quite volatile in nature and the right choice of multibaggers may prove to be wealth creators for the general public. Investors may look for the derived factors for investing their savings into profitable channels by picking up those stocks which may prove to be multibaggers in near future. The development of a model for the identification of factors affecting the choice of multibaggers in the securities market is the original contribution of the authors.</p></div>","PeriodicalId":54095,"journal":{"name":"Asia-Pacific Financial Markets","volume":"30 4","pages":"677 - 699"},"PeriodicalIF":2.6000,"publicationDate":"2022-11-16","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"1","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Asia-Pacific Financial Markets","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s10690-022-09394-4","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 1

Abstract

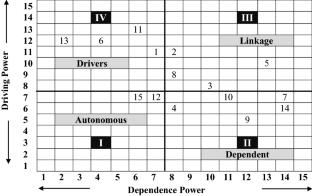

The purpose of this study is to explore the factors affecting the selection of multibagger stocks in the securities market. Further, the study aims to develop a model using interpretive structural modeling (ISM). Thereafter, the driving and dependence power of factors was found using matriced impact croises multiplication appliquee a un classement (MICMAC). A group of financial analysts and academic experts having experience in dealing in the Indian securities market were consulted and interpretive structural modelling (ISM) is adopted to develop the contextual relationship among various factors for each dimension of multibagger stocks selection. Further, to identify the driving and the dependence power of factors, the results of the ISM are used as an input to MICMAC analysis. The results of the study indicate the large potential market (C11), visionary leader (C13), unique business model (C6), understanding of the sector (C1), and promoter and management capability (C2) are the dominant factors. MICMAC analysis indicates that driving, dependent and linkage factors are 4, 5, and 4 respectively. The factors obtained for ISM model development and MICMAC analysis are based on the experts’ opinions. As it is a subjective judgment, there are chances of biasness on basis of personal opinions. A questionnaire survey can be conducted to gather viewpoints on these factors from more financial experts and portfolio consultants. The study has been executed in discussion with financial analysts and academic experts having experience in dealing in the securities market. Hence, derived results have practical validity. The securities market is quite volatile in nature and the right choice of multibaggers may prove to be wealth creators for the general public. Investors may look for the derived factors for investing their savings into profitable channels by picking up those stocks which may prove to be multibaggers in near future. The development of a model for the identification of factors affecting the choice of multibaggers in the securities market is the original contribution of the authors.

期刊介绍:

The current remarkable growth in the Asia-Pacific financial markets is certain to continue. These markets are expected to play a further important role in the world capital markets for investment and risk management. In accordance with this development, Asia-Pacific Financial Markets (formerly Financial Engineering and the Japanese Markets), the official journal of the Japanese Association of Financial Econometrics and Engineering (JAFEE), is expected to provide an international forum for researchers and practitioners in academia, industry, and government, who engage in empirical and/or theoretical research into the financial markets. We invite submission of quality papers on all aspects of finance and financial engineering.

Here we interpret the term ''financial engineering'' broadly enough to cover such topics as financial time series, portfolio analysis, global asset allocation, trading strategy for investment, optimization methods, macro monetary economic analysis and pricing models for various financial assets including derivatives We stress that purely theoretical papers, as well as empirical studies that use Asia-Pacific market data, are welcome.

Officially cited as: Asia-Pac Financ Markets

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: