Investor sentiment and the risk–return relation: A two-in-one approach

IF 2.1

3区 经济学

Q2 BUSINESS, FINANCE

引用次数: 0

Abstract

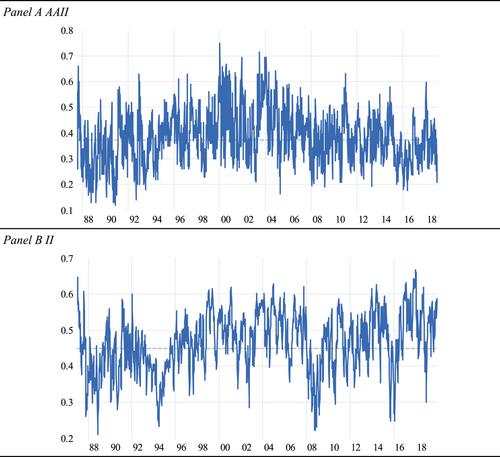

Traditional finance theory posits a positive risk–return relation, but empirical evidence is inconclusive. Retail investor sentiment has long been viewed as a distorting factor, while more recently institutional investor sentiment is thought to play a role. We examine the separate and joint impacts of retail and institutional investor sentiments on the risk-return relation. We find, at both market and firm levels, the risk-return relation is more likely to be distorted by the two investor-type sentiments jointly, rather than separately. We further find a cross-sectional pattern, with the risk-return relation being more sensitive to investor sentiment for stocks with specific characteristics.

投资者情绪与风险回报关系:二合一方法

传统金融理论认为风险与收益之间存在正相关关系,但经验证据并不确定。长期以来,散户投资者的情绪一直被视为一个扭曲因素,而最近机构投资者的情绪也被认为起到了一定作用。我们研究了散户和机构投资者情绪对风险收益关系的单独和共同影响。我们发现,在市场和公司层面,风险收益关系更有可能被这两种投资者类型的情绪共同扭曲,而不是单独扭曲。我们还发现了一种横截面模式,即具有特定特征的股票的风险收益关系对投资者情绪更为敏感。

本文章由计算机程序翻译,如有差异,请以英文原文为准。

求助全文

约1分钟内获得全文

求助全文

来源期刊

European Financial Management

BUSINESS, FINANCE-

CiteScore

4.30

自引率

18.20%

发文量

60

期刊介绍:

European Financial Management publishes the best research from around the world, providing a forum for both academics and practitioners concerned with the financial management of modern corporation and financial institutions. The journal publishes signficant new finance research on timely issues and highlights key trends in Europe in a clear and accessible way, with articles covering international research and practice that have direct or indirect bearing on Europe.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: