{"title":"Does Market Performance (Tobin’s Q) Have A Negative Effect On Credit Ratings? Evidence From South Korea","authors":"Hyoung-Joo Lim, Dafydd Mali","doi":"10.1007/s10690-023-09406-x","DOIUrl":null,"url":null,"abstract":"<div><p>Tobin’s Q is an established measure of firm performance, based on investor confidence. However, the association between Tobin’s Q and credit ratings is not well-established in the literature. Using a sample of Korean listed firms over the 2001–2016 sample period, Probit regression analysis shows that overall, Tobin’s Q is positively associated with credit ratings. However, for firms with a > 1 (1 <) Tobin’s Q ratio, a negative (positive) relationship exists. Moreover, in independent regressions, a threshold level if found where the effect of Tobin’s Q on credit ratings changes from being positive (0.2), to negative (0.3). To the best of our knowledge, we are the first to demonstrate that credit rating agencies are nuanced when making default risk assessments. Specifically, that in South Korea, a threshold level exists, at which increasing Tobin’s Q values reduce credit ratings. Empirical evidence of the different association between Tobin’s Q (market confidence) and credit ratings can extend the literature and offer insights to market participants. Furthermore, because Tobin’s Q is a commonly used proxy for financial performance in accounting lectures, the study has practical implications for academics in classrooms.</p></div>","PeriodicalId":54095,"journal":{"name":"Asia-Pacific Financial Markets","volume":"31 1","pages":"53 - 80"},"PeriodicalIF":2.6000,"publicationDate":"2023-05-10","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://link.springer.com/content/pdf/10.1007/s10690-023-09406-x.pdf","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Asia-Pacific Financial Markets","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s10690-023-09406-x","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

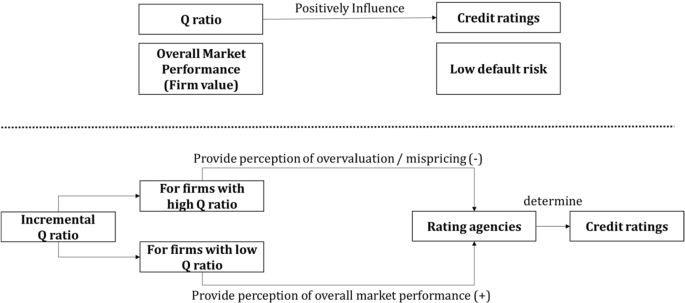

Tobin’s Q is an established measure of firm performance, based on investor confidence. However, the association between Tobin’s Q and credit ratings is not well-established in the literature. Using a sample of Korean listed firms over the 2001–2016 sample period, Probit regression analysis shows that overall, Tobin’s Q is positively associated with credit ratings. However, for firms with a > 1 (1 <) Tobin’s Q ratio, a negative (positive) relationship exists. Moreover, in independent regressions, a threshold level if found where the effect of Tobin’s Q on credit ratings changes from being positive (0.2), to negative (0.3). To the best of our knowledge, we are the first to demonstrate that credit rating agencies are nuanced when making default risk assessments. Specifically, that in South Korea, a threshold level exists, at which increasing Tobin’s Q values reduce credit ratings. Empirical evidence of the different association between Tobin’s Q (market confidence) and credit ratings can extend the literature and offer insights to market participants. Furthermore, because Tobin’s Q is a commonly used proxy for financial performance in accounting lectures, the study has practical implications for academics in classrooms.

期刊介绍:

The current remarkable growth in the Asia-Pacific financial markets is certain to continue. These markets are expected to play a further important role in the world capital markets for investment and risk management. In accordance with this development, Asia-Pacific Financial Markets (formerly Financial Engineering and the Japanese Markets), the official journal of the Japanese Association of Financial Econometrics and Engineering (JAFEE), is expected to provide an international forum for researchers and practitioners in academia, industry, and government, who engage in empirical and/or theoretical research into the financial markets. We invite submission of quality papers on all aspects of finance and financial engineering.

Here we interpret the term ''financial engineering'' broadly enough to cover such topics as financial time series, portfolio analysis, global asset allocation, trading strategy for investment, optimization methods, macro monetary economic analysis and pricing models for various financial assets including derivatives We stress that purely theoretical papers, as well as empirical studies that use Asia-Pacific market data, are welcome.

Officially cited as: Asia-Pac Financ Markets

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: