The COVID-19 risk in the Chinese option market

IF 1.8

4区 经济学

Q2 BUSINESS, FINANCE

引用次数: 5

Abstract

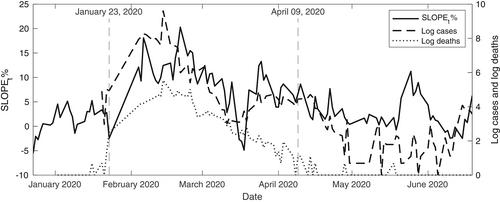

The COVID-19 pandemic has increased fear of a financial market crash in China. We use an implied volatility slope measure, which proxies the cost of option protection against and therefore trader's fear of crash risk, using the Shanghai Shenzhen CSI 300 Index options. We show that this measure is positively related to new cases and deaths of the pandemic during the COVID-19 outbreak in China. Option traders are willing to pay more for hedging downside tail risk as the pandemic worsens, and are no longer as concerned by news of cases and deaths after the lift of the lockdown.

中国期权市场的新冠肺炎风险

摘要新冠肺炎疫情加剧了人们对中国金融市场崩溃的担忧。我们使用隐含波动率斜率度量,使用沪深沪深300指数期权,该度量代表期权保护的成本,从而代表交易员对崩溃风险的恐惧。我们表明,这一措施与2019冠状病毒病在中国爆发期间的新冠肺炎病例和死亡呈正相关。随着疫情的恶化,期权交易员愿意为对冲下行尾部风险支付更多费用,并且在解除封锁后不再那么担心病例和死亡的消息。

本文章由计算机程序翻译,如有差异,请以英文原文为准。

求助全文

约1分钟内获得全文

求助全文

来源期刊

International Review of Finance

BUSINESS, FINANCE-

CiteScore

3.30

自引率

5.90%

发文量

28

期刊介绍:

The International Review of Finance (IRF) publishes high-quality research on all aspects of financial economics, including traditional areas such as asset pricing, corporate finance, market microstructure, financial intermediation and regulation, financial econometrics, financial engineering and risk management, as well as new areas such as markets and institutions of emerging market economies, especially those in the Asia-Pacific region. In addition, the Letters Section in IRF is a premium outlet of letter-length research in all fields of finance. The length of the articles in the Letters Section is limited to a maximum of eight journal pages.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: