{"title":"Direct cost analysis for 32,783 samples with preanalytical phase errors.","authors":"Pinar Eker","doi":"10.14744/nci.2022.73555","DOIUrl":null,"url":null,"abstract":"<p><strong>Objective: </strong>Errors in the laboratory process often occur in the preanalytical phase (PA). The study aims to calculate the direct cost elements of PA errors, including material, logistics, transfer, personnel workforce, and medical waste.</p><p><strong>Methods: </strong>Medical laboratory PA phase errors were retrospectively reviewed using the Laboratory Information Management System. We evaluated the whole 2019 laboratory data of the 836-bed Health Sciences University Umraniye Training and Research Hospital (UTRH). We assessed the direct cost elements of PA errors, such as those related to material, logistics, transfer, human resources, and waste. We performed the procedure for both samples analyzed in the hospital and transferred to the central laboratory.</p><p><strong>Results: </strong>We analyzed 1,939,650 patient samples and 46,534,532 parameters studied in 2019 for UTRH. The rates for rejected tests and rejected samples (tube) for UTRH were noted as 0.32% and 1.7%, respectively. The total direct cost for PA errors was TRY 438,284.51 (68,918.07 euros) for 32,783 patient samples and 147,893 tests. We calculated the total cost for PA test errors detected in the hospital as TRY 390,238.06, while the total cost for PA test errors detected in the central laboratory was TRY 48,046.45. 89% of the total cost was for PA errors detected in the hospital, and 11% was for the errors detected in the central laboratory. The 2019 direct PA error cost we calculated based on our hospital's data was 0.153% of the 2019 hospital operating cost. We calculated the direct cost per rejected sample as TRY 13.37 (2.1 Euro).</p><p><strong>Conclusion: </strong>Providing reliable laboratory service with the least possible financial loss is one of the main goals in terms of laboratory medicine. In achieving this goal, the prevention of error costs is a priority. The direct cost elements for the PA phase, where laboratory errors are concentrated, can be easily identified. The amount of PA phase error direct cost will attract the attention of health policy decision-makers and field professionals and inspire further research. Therefore, we tried to determine a threshold cost regarding interventions and practices required to prevent PA phase errors.</p>","PeriodicalId":19164,"journal":{"name":"Northern Clinics of Istanbul","volume":"9 4","pages":"391-400"},"PeriodicalIF":0.9000,"publicationDate":"2022-09-05","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://ftp.ncbi.nlm.nih.gov/pub/pmc/oa_pdf/a6/95/NCI-9-391.PMC9514066.pdf","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Northern Clinics of Istanbul","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.14744/nci.2022.73555","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2022/1/1 0:00:00","PubModel":"eCollection","JCR":"Q3","JCRName":"MEDICINE, GENERAL & INTERNAL","Score":null,"Total":0}

引用次数: 0

Abstract

Objective: Errors in the laboratory process often occur in the preanalytical phase (PA). The study aims to calculate the direct cost elements of PA errors, including material, logistics, transfer, personnel workforce, and medical waste.

Methods: Medical laboratory PA phase errors were retrospectively reviewed using the Laboratory Information Management System. We evaluated the whole 2019 laboratory data of the 836-bed Health Sciences University Umraniye Training and Research Hospital (UTRH). We assessed the direct cost elements of PA errors, such as those related to material, logistics, transfer, human resources, and waste. We performed the procedure for both samples analyzed in the hospital and transferred to the central laboratory.

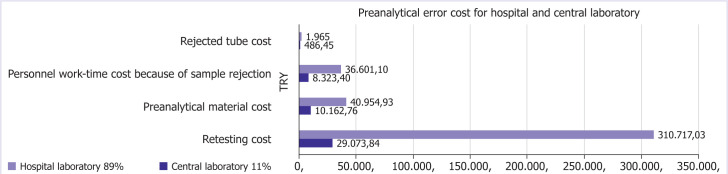

Results: We analyzed 1,939,650 patient samples and 46,534,532 parameters studied in 2019 for UTRH. The rates for rejected tests and rejected samples (tube) for UTRH were noted as 0.32% and 1.7%, respectively. The total direct cost for PA errors was TRY 438,284.51 (68,918.07 euros) for 32,783 patient samples and 147,893 tests. We calculated the total cost for PA test errors detected in the hospital as TRY 390,238.06, while the total cost for PA test errors detected in the central laboratory was TRY 48,046.45. 89% of the total cost was for PA errors detected in the hospital, and 11% was for the errors detected in the central laboratory. The 2019 direct PA error cost we calculated based on our hospital's data was 0.153% of the 2019 hospital operating cost. We calculated the direct cost per rejected sample as TRY 13.37 (2.1 Euro).

Conclusion: Providing reliable laboratory service with the least possible financial loss is one of the main goals in terms of laboratory medicine. In achieving this goal, the prevention of error costs is a priority. The direct cost elements for the PA phase, where laboratory errors are concentrated, can be easily identified. The amount of PA phase error direct cost will attract the attention of health policy decision-makers and field professionals and inspire further research. Therefore, we tried to determine a threshold cost regarding interventions and practices required to prevent PA phase errors.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: