{"title":"Deep diving into the S&P Europe 350 index network and its reaction to COVID-19.","authors":"Ariana Paola Cortés Ángel, Mustafa Hakan Eratalay","doi":"10.1007/s42001-022-00172-w","DOIUrl":null,"url":null,"abstract":"<p><p>In this paper, we analyse the dynamic partial correlation network of the constituent stocks of S&P Europe 350. We focus on global parameters such as radius, which is rarely used in financial networks literature, and also the diameter and distance parameters. The first two parameters are useful for deducing the force that economic instability should exert to trigger a cascade effect on the network. With these global parameters, we hone the boundaries of the strength that a shock should exert to trigger a cascade effect. In addition, we analysed the homophilic profiles, which is quite new in financial networks literature. We found highly homophilic relationships among companies, considering firms by country and industry. We also calculate the local parameters such as degree, closeness, betweenness, eigenvector, and harmonic centralities to gauge the importance of the companies regarding different aspects, such as the strength of the relationships with their neighbourhood and their location in the network. Finally, we analysed a network substructure by introducing the skeleton concept of a dynamic network. This subnetwork allowed us to study the stability of relations among constituents and detect a significant increase in these stable connections during the Covid-19 pandemic.</p>","PeriodicalId":29946,"journal":{"name":"Journal of Computational Social Science","volume":" ","pages":"1343-1408"},"PeriodicalIF":2.3000,"publicationDate":"2022-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9244332/pdf/","citationCount":"3","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Computational Social Science","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s42001-022-00172-w","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2022/6/28 0:00:00","PubModel":"Epub","JCR":"Q2","JCRName":"SOCIAL SCIENCES, MATHEMATICAL METHODS","Score":null,"Total":0}

引用次数: 3

Abstract

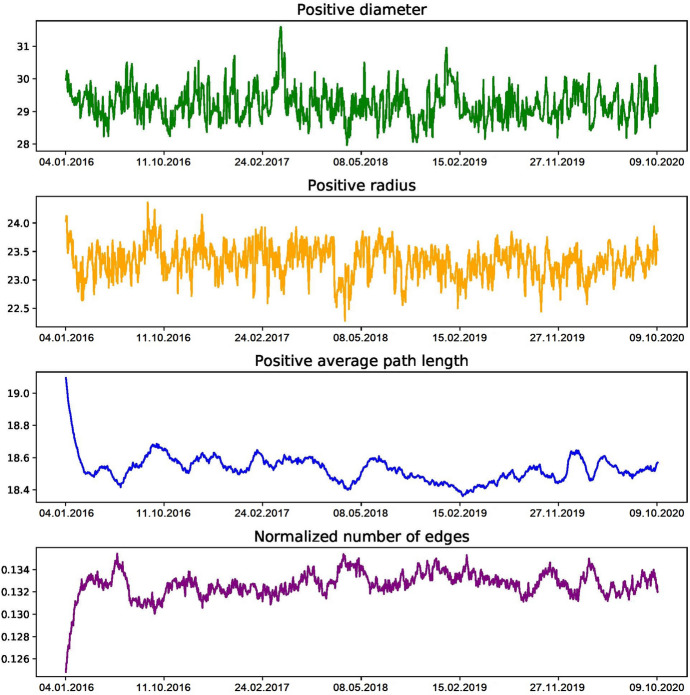

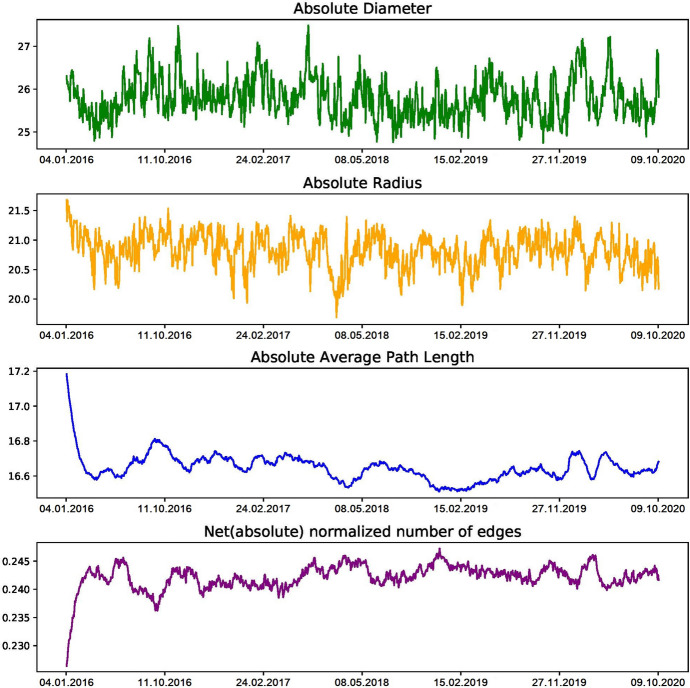

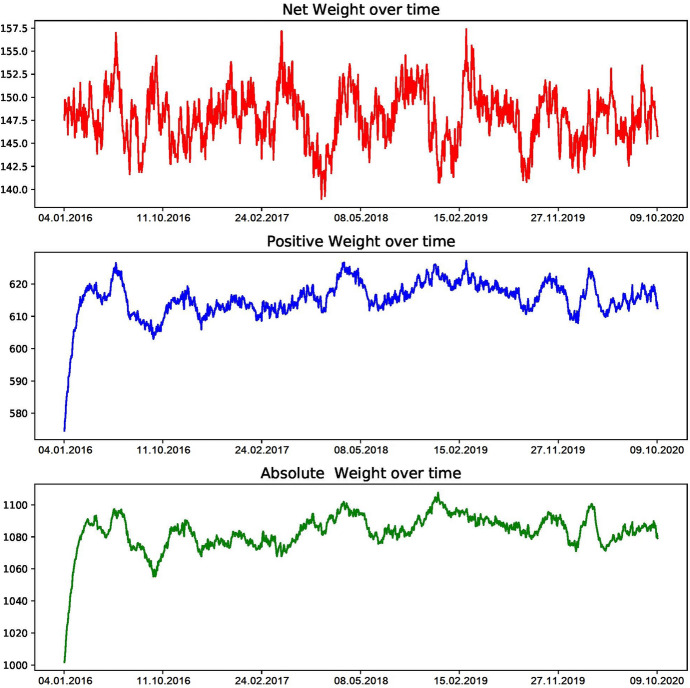

In this paper, we analyse the dynamic partial correlation network of the constituent stocks of S&P Europe 350. We focus on global parameters such as radius, which is rarely used in financial networks literature, and also the diameter and distance parameters. The first two parameters are useful for deducing the force that economic instability should exert to trigger a cascade effect on the network. With these global parameters, we hone the boundaries of the strength that a shock should exert to trigger a cascade effect. In addition, we analysed the homophilic profiles, which is quite new in financial networks literature. We found highly homophilic relationships among companies, considering firms by country and industry. We also calculate the local parameters such as degree, closeness, betweenness, eigenvector, and harmonic centralities to gauge the importance of the companies regarding different aspects, such as the strength of the relationships with their neighbourhood and their location in the network. Finally, we analysed a network substructure by introducing the skeleton concept of a dynamic network. This subnetwork allowed us to study the stability of relations among constituents and detect a significant increase in these stable connections during the Covid-19 pandemic.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: