{"title":"The complex nature of financial market microstructure: the case of a stock market crash.","authors":"Feng Shi, John Paul Broussard, G Geoffrey Booth","doi":"10.1007/s11403-021-00343-4","DOIUrl":null,"url":null,"abstract":"<p><p>This paper uses multivariate Hawkes processes to model the transactions behavior of the US stock market as measured by the 30 Dow Jones Industrial Average individual stocks before, during and after the 36-min May 6, 2010, Flash Crash. The basis for our analysis is the excitation matrix, which describes a complex network of interactions among the stocks. Using high-frequency transactions data, we find strong evidence of self- and asymmetrically cross-induced contagion and the presence of fragmented trading venues. Our findings have implications for stock trading and corresponding risk management strategies as well as stock market microstructure design.</p>","PeriodicalId":45479,"journal":{"name":"Journal of Economic Interaction and Coordination","volume":" ","pages":"1-40"},"PeriodicalIF":1.0000,"publicationDate":"2022-01-04","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC8724601/pdf/","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Economic Interaction and Coordination","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s11403-021-00343-4","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

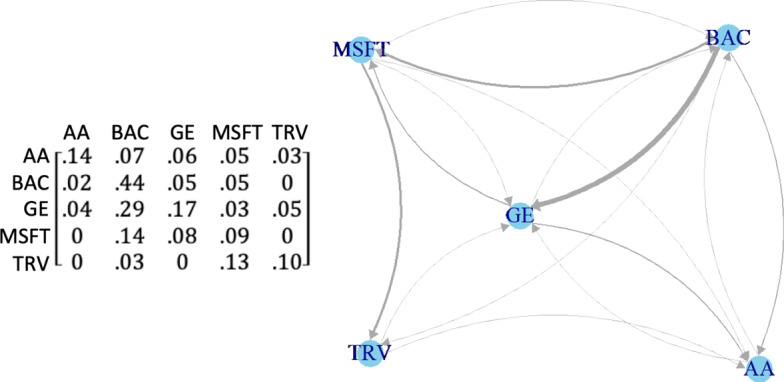

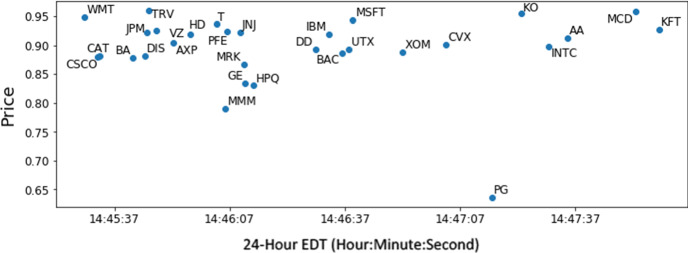

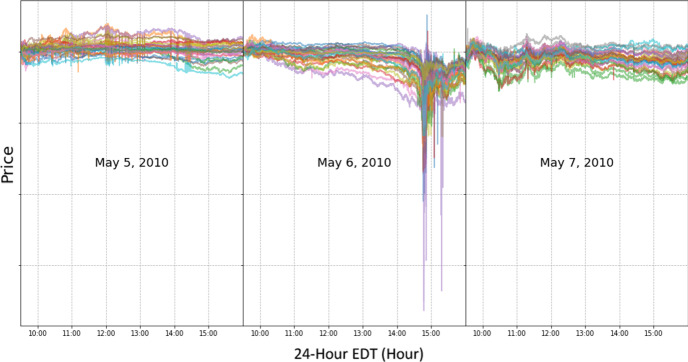

This paper uses multivariate Hawkes processes to model the transactions behavior of the US stock market as measured by the 30 Dow Jones Industrial Average individual stocks before, during and after the 36-min May 6, 2010, Flash Crash. The basis for our analysis is the excitation matrix, which describes a complex network of interactions among the stocks. Using high-frequency transactions data, we find strong evidence of self- and asymmetrically cross-induced contagion and the presence of fragmented trading venues. Our findings have implications for stock trading and corresponding risk management strategies as well as stock market microstructure design.

期刊介绍:

Journal of Economic Interaction and Coordination addresses the vibrant and interdisciplinary field of agent-based approaches to economics and social sciences.

It focuses on simulating and synthesizing emergent phenomena and collective behavior in order to understand economic and social systems. Relevant topics include, but are not limited to, the following: markets as complex adaptive systems, multi-agents in economics, artificial markets with heterogeneous agents, financial markets with heterogeneous agents, theory and simulation of agent-based models, adaptive agents with artificial intelligence, interacting particle systems in economics, social and complex networks, econophysics, non-linear economic dynamics, evolutionary games, market mechanisms in distributed computing systems, experimental economics, collective decisions.

Contributions are mostly from economics, physics, computer science and related fields and are typically based on sound theoretical models and supported by experimental validation. Survey papers are also welcome.

Journal of Economic Interaction and Coordination is the official journal of the Association of Economic Science with Heterogeneous Interacting Agents.

Officially cited as: J Econ Interact Coord

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: