{"title":"Ethical perspectives of certified public accountants and the cannabis industry.","authors":"G Suzanne Owens-Ott, Johnny Snyder, Richard Ott","doi":"10.1186/s42238-022-00118-z","DOIUrl":null,"url":null,"abstract":"<p><strong>Background: </strong>Certified public accountants must follow very high standards of ethical conduct as set forth by the AICPA Code of Professional Conduct and individual state licensing requirements. A 2019 grounded theory qualitative study posed that CPAs remain largely hesitant to serve the cannabis industry primarily because they fear federal prosecution as long as cannabis remains on the DEA's Schedule I Drug List. The purpose of this research was to determine the perceptions of CPAs regarding providing accounting services to the cannabis industry in states that have legalized cannabis usage. This study investigated whether CPAs would serve the industry, why they might decline to serve the industry, what risks they believe serving the industry posed, and whether they believe serving the cannabis industry would create a moral or ethical issue.</p><p><strong>Methods: </strong>This follow-up quantitative study investigated a small convenience sample of approximately one hundred CPAs in Colorado and Washington to learn more about their perceptions of serving the cannabis industry. Data was analyzed using chi-square and Mann-Whitney U tests to determine if there were any differences in perceptions between groups such as states, gender, and age categories.</p><p><strong>Results: </strong>Of the participants, 77% responded that neither they nor their firm provided services to a cannabis-related business client compared to 23% that did serve cannabis clients. More Colorado CPAs were willing to turn down CRB work than were expected and fewer Colorado CPAs would be willing to take on CRB clients than were expected. While in Washington, fewer CPAs would turn down RB clients than expected, and more are willing to accept CRB clients than were expected. The risk due to potential liability coverage issues due to serving the cannabis industry was rated the highest while the risk of losing the CPA license was rated lowest. Data indicated that there was not a statistically significant difference between Colorado and Washington participants related to whether they were morally or religiously opposed to working in the industry or if they viewed serving the industry as an ethical violation.</p><p><strong>Conclusion: </strong>CPAs remain largely unwilling to serve the cannabis industry primarily because CPAs fear federal prosecution as long as cannabis remains on the DEA's Schedule I Drug Listing. The results of this study indicate that while most CPAs are not morally or religiously opposed to serving the industry, about half still believe doing so may constitute an ethical violation for a CPA.</p>","PeriodicalId":15172,"journal":{"name":"Journal of Cannabis Research","volume":" ","pages":"8"},"PeriodicalIF":0.0000,"publicationDate":"2022-01-26","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC8790865/pdf/","citationCount":"1","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Cannabis Research","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1186/s42238-022-00118-z","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

引用次数: 1

Abstract

Background: Certified public accountants must follow very high standards of ethical conduct as set forth by the AICPA Code of Professional Conduct and individual state licensing requirements. A 2019 grounded theory qualitative study posed that CPAs remain largely hesitant to serve the cannabis industry primarily because they fear federal prosecution as long as cannabis remains on the DEA's Schedule I Drug List. The purpose of this research was to determine the perceptions of CPAs regarding providing accounting services to the cannabis industry in states that have legalized cannabis usage. This study investigated whether CPAs would serve the industry, why they might decline to serve the industry, what risks they believe serving the industry posed, and whether they believe serving the cannabis industry would create a moral or ethical issue.

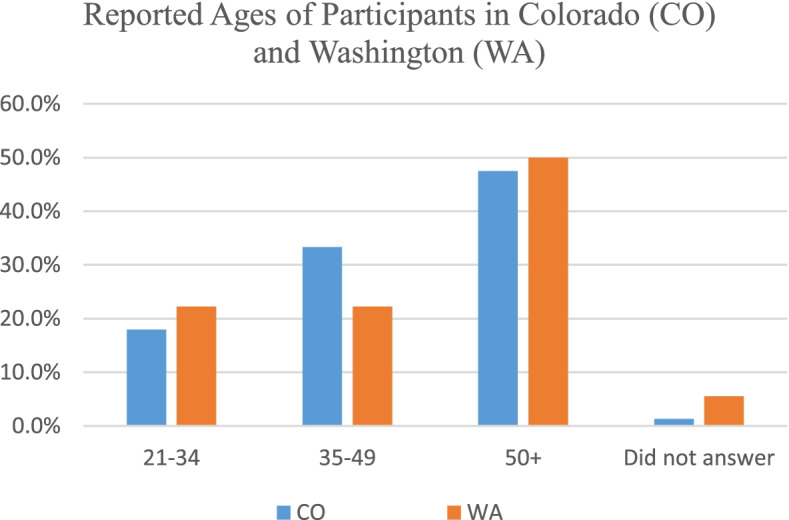

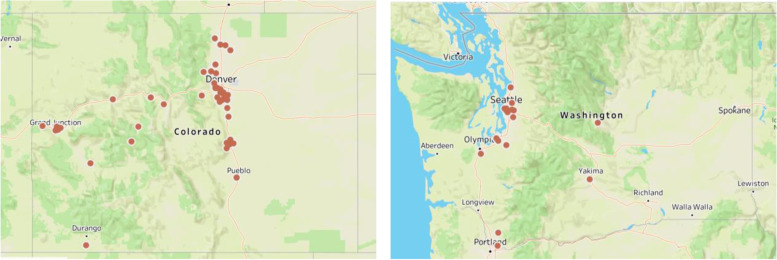

Methods: This follow-up quantitative study investigated a small convenience sample of approximately one hundred CPAs in Colorado and Washington to learn more about their perceptions of serving the cannabis industry. Data was analyzed using chi-square and Mann-Whitney U tests to determine if there were any differences in perceptions between groups such as states, gender, and age categories.

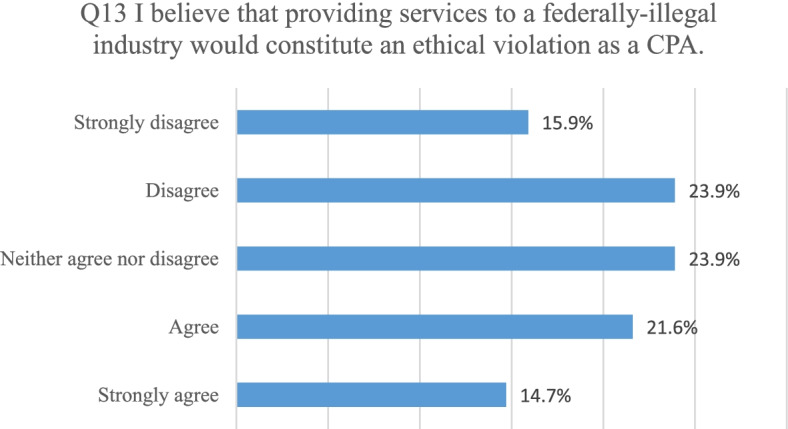

Results: Of the participants, 77% responded that neither they nor their firm provided services to a cannabis-related business client compared to 23% that did serve cannabis clients. More Colorado CPAs were willing to turn down CRB work than were expected and fewer Colorado CPAs would be willing to take on CRB clients than were expected. While in Washington, fewer CPAs would turn down RB clients than expected, and more are willing to accept CRB clients than were expected. The risk due to potential liability coverage issues due to serving the cannabis industry was rated the highest while the risk of losing the CPA license was rated lowest. Data indicated that there was not a statistically significant difference between Colorado and Washington participants related to whether they were morally or religiously opposed to working in the industry or if they viewed serving the industry as an ethical violation.

Conclusion: CPAs remain largely unwilling to serve the cannabis industry primarily because CPAs fear federal prosecution as long as cannabis remains on the DEA's Schedule I Drug Listing. The results of this study indicate that while most CPAs are not morally or religiously opposed to serving the industry, about half still believe doing so may constitute an ethical violation for a CPA.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: