{"title":"The evolution from life insurance to financial engineering.","authors":"Ralph S J Koijen, Motohiro Yogo","doi":"10.1057/s10713-021-00068-1","DOIUrl":null,"url":null,"abstract":"<p><p>Since the mid-1980s, the share of household net worth intermediated by US financial institutions has shifted from defined benefit plans to life insurers and defined contribution plans. Life insurers have primarily grown through variable annuities, which are mutual funds with longevity insurance, a potential tax advantage, and minimum return guarantees. The minimum return guarantees change the primary function of life insurers from traditional insurance to financial engineering. Variable annuity insurers are exposed to interest and equity risk mismatch and their stock returns were especially low during the COVID-19 crisis. We consider regulatory changes, such as more detailed financial disclosure and standardized stress tests, to monitor potential risk mismatch and to ensure stability of the insurance sector.</p>","PeriodicalId":507077,"journal":{"name":"The Geneva Risk and Insurance Review","volume":"46 2","pages":"89-111"},"PeriodicalIF":0.0000,"publicationDate":"2021-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC8377459/pdf/","citationCount":"6","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"The Geneva Risk and Insurance Review","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1057/s10713-021-00068-1","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2021/8/20 0:00:00","PubModel":"Epub","JCR":"","JCRName":"","Score":null,"Total":0}

引用次数: 6

Abstract

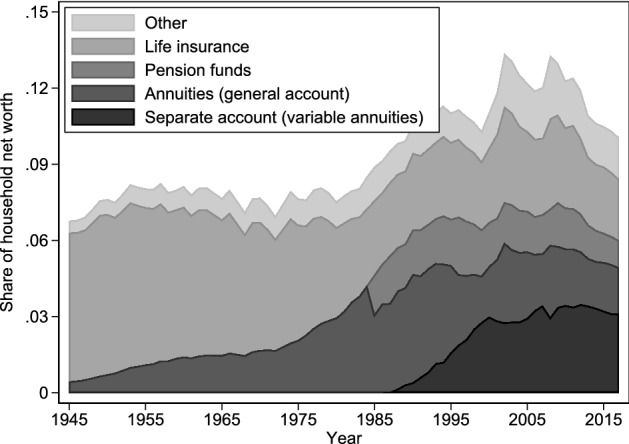

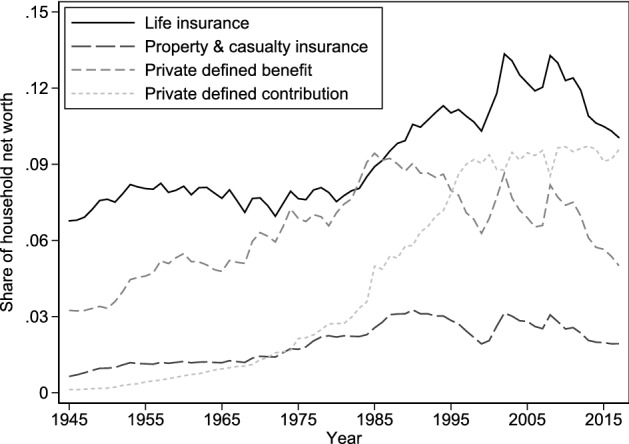

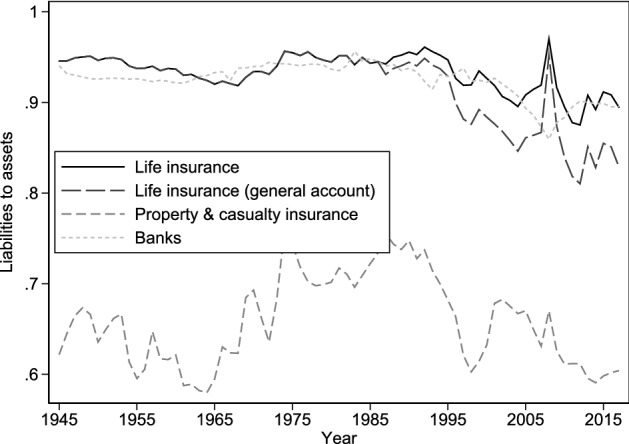

Since the mid-1980s, the share of household net worth intermediated by US financial institutions has shifted from defined benefit plans to life insurers and defined contribution plans. Life insurers have primarily grown through variable annuities, which are mutual funds with longevity insurance, a potential tax advantage, and minimum return guarantees. The minimum return guarantees change the primary function of life insurers from traditional insurance to financial engineering. Variable annuity insurers are exposed to interest and equity risk mismatch and their stock returns were especially low during the COVID-19 crisis. We consider regulatory changes, such as more detailed financial disclosure and standardized stress tests, to monitor potential risk mismatch and to ensure stability of the insurance sector.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: