{"title":"Credit contingent interest rate swap pricing.","authors":"Haohan Huang, Huaxiong Huang, Eugene Wang, Hongmei Zhu","doi":"10.1186/s40929-017-0015-x","DOIUrl":null,"url":null,"abstract":"<p><p>Credit value adjustment (CVA) is an adjustment to an existing trading price based on the counterparty-risk premium. Currently, CVA is computed with an implicit assumption that the replacement contract is default-free after the original counterparty defaults, with the assumption that those trades will not re-assigned. In the actual counterparty default settlement, it is the norm that trades will be re-assigned, especially on the buy side. Since the counterparty of the replacement contract could also default within the lifetime of an existing contract, ignoring the possibility of counterparty defaults of replacement contracts will either under or over estimate the cost of the risk. An important practical question is, therefore, how to estimate under/over pricing of CVA under current practice. In this paper, we considered the pricing of credit contingent interest rate swap (CCIRS) or credit contingent default swap (CCDS), which is considered the CVA hedge for interest rate swaps (IRS). We derived partial differential Eqs. (PDEs) satisfied by the approximated CVA with the assumption that the replacement contracts do not default. For comparison purposes, we also derived the PDEs for the cost of CVA by relaxing the assumption of default-free replacement contracts with a finite number of counterparty defaults. It shows that the no-default and two default cases can be derived within the same analytical solution framework, similar to the Funding Valuation Adjustment (FVA) problem where continuous funding is a reasonable assumption. The finite number of default case is non-trivial. The PDE for the two default case is derived in this paper. We calibrate our model based on market data and carry out extensive computations for the purpose of comparing these three CVAs. Our basic finding is that the values of the two CVAs are close for top rated counterparties. On the other hand, for counterparties with lower credit ratings, the difference among the two CVAs can be significant.</p>","PeriodicalId":91926,"journal":{"name":"Mathematics-in-industry case studies","volume":"8 1","pages":"6"},"PeriodicalIF":0.0000,"publicationDate":"2017-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://sci-hub-pdf.com/10.1186/s40929-017-0015-x","citationCount":"1","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Mathematics-in-industry case studies","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1186/s40929-017-0015-x","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2017/10/3 0:00:00","PubModel":"Epub","JCR":"","JCRName":"","Score":null,"Total":0}

引用次数: 1

Abstract

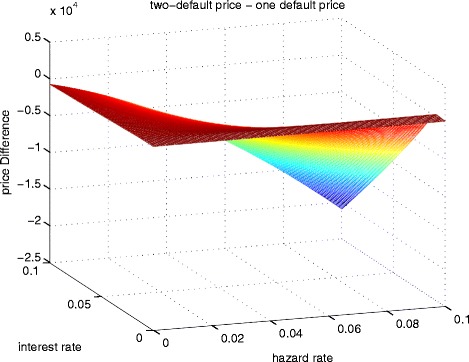

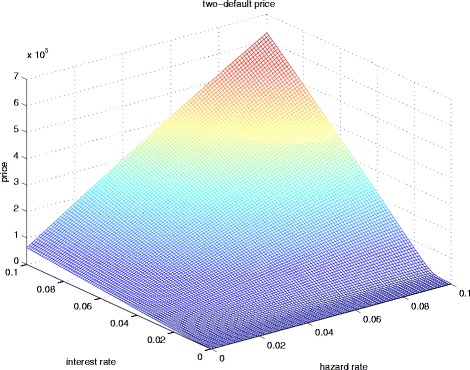

Credit value adjustment (CVA) is an adjustment to an existing trading price based on the counterparty-risk premium. Currently, CVA is computed with an implicit assumption that the replacement contract is default-free after the original counterparty defaults, with the assumption that those trades will not re-assigned. In the actual counterparty default settlement, it is the norm that trades will be re-assigned, especially on the buy side. Since the counterparty of the replacement contract could also default within the lifetime of an existing contract, ignoring the possibility of counterparty defaults of replacement contracts will either under or over estimate the cost of the risk. An important practical question is, therefore, how to estimate under/over pricing of CVA under current practice. In this paper, we considered the pricing of credit contingent interest rate swap (CCIRS) or credit contingent default swap (CCDS), which is considered the CVA hedge for interest rate swaps (IRS). We derived partial differential Eqs. (PDEs) satisfied by the approximated CVA with the assumption that the replacement contracts do not default. For comparison purposes, we also derived the PDEs for the cost of CVA by relaxing the assumption of default-free replacement contracts with a finite number of counterparty defaults. It shows that the no-default and two default cases can be derived within the same analytical solution framework, similar to the Funding Valuation Adjustment (FVA) problem where continuous funding is a reasonable assumption. The finite number of default case is non-trivial. The PDE for the two default case is derived in this paper. We calibrate our model based on market data and carry out extensive computations for the purpose of comparing these three CVAs. Our basic finding is that the values of the two CVAs are close for top rated counterparties. On the other hand, for counterparties with lower credit ratings, the difference among the two CVAs can be significant.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: