{"title":"Exploring Macroeconomic Determinants of Housing Bubbles: New Evidence from Dynamic Panel Probit Models","authors":"Shu-hen Chiang, Chien-Fu Chen","doi":"10.1007/s11293-025-09820-8","DOIUrl":null,"url":null,"abstract":"<div><p>Since the 2008 global financial crisis, the detection of housing bubbles has attracted unprecedented attention. By using price-to-rent data collected from the Organization for Economic Co-operation and Development, this paper adopts the Phillips et al<i>.</i> right-tailed unit root tests to identify housing bubbles across the Group of Seven countries from the first quarter of 1970 to the second quarter of 2021. In addition, a novel estimation approach (the dynamic panel probit model) was employed to take account of the bubble persistence and explore the macroeconomic determinants driving the housing bubbles. The empirical results indicate that each country experienced episodes of housing bubbles and the bubble clusters appeared in two phases, namely, 2003–2008 and post-2016. More importantly, there is evidence that certain macroeconomic variables drove the housing bubbles, especially a low interest rate and rapidly-growing money supply. The policy implication of this study is that central banks implementing ultra-loose monetary policy need to take housing bubble risk into careful consideration.</p></div>","PeriodicalId":46061,"journal":{"name":"ATLANTIC ECONOMIC JOURNAL","volume":"53 1-2","pages":"3 - 17"},"PeriodicalIF":0.8000,"publicationDate":"2025-05-12","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"ATLANTIC ECONOMIC JOURNAL","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s11293-025-09820-8","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q4","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

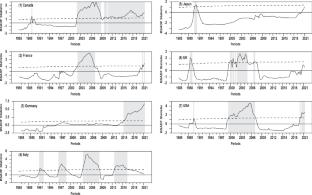

Since the 2008 global financial crisis, the detection of housing bubbles has attracted unprecedented attention. By using price-to-rent data collected from the Organization for Economic Co-operation and Development, this paper adopts the Phillips et al. right-tailed unit root tests to identify housing bubbles across the Group of Seven countries from the first quarter of 1970 to the second quarter of 2021. In addition, a novel estimation approach (the dynamic panel probit model) was employed to take account of the bubble persistence and explore the macroeconomic determinants driving the housing bubbles. The empirical results indicate that each country experienced episodes of housing bubbles and the bubble clusters appeared in two phases, namely, 2003–2008 and post-2016. More importantly, there is evidence that certain macroeconomic variables drove the housing bubbles, especially a low interest rate and rapidly-growing money supply. The policy implication of this study is that central banks implementing ultra-loose monetary policy need to take housing bubble risk into careful consideration.

期刊介绍:

The Atlantic Economic Journal (AEJ) has an international reputation for excellent articles in all interest areas, without regard to fields or methodological preferences. Founded in 1973 by the International Atlantic Economic Society, a need was identified for increased communication among scholars from different countries. For over 30 years, the AEJ has continuously sought articles that traced some of the most critical economic changes and developments to occur on the global level. The journal''s goal is to facilitate and synthesize economic research across nations to encourage cross-fertilization of ideas and scholarly research. Contributors include some of the world''s most respected economists and financial specialists, including Nobel laureates and leading government officials. AEJ welcomes both theoretical and empirical articles, as well as public policy papers. All manuscripts are submitted to a double-blind peer review process. In addition to formal publication of full-length articles, the AEJ provides an opportunity for less formal communication through its Anthology section. A small point may not be worthy of a full-length, formal paper but is important enough to warrant dissemination to other researchers. Research in progress may be of interest to other scholars in the field. A research approach ending in negative results needs to be shared to save others similar pitfalls. The Anthology section has been established to facilitate these forms of communication. Anthologies provide a means by which short manuscripts of less than 500 words can quickly appear in the AEJ. All submissions are formally reviewed by the Board of Editors. Officially cited as: Atl Econ J

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: