On The Continuous Statistical Maxwell Distribution for Obtaining the Risk in Economy

IF 2.9

4区 工程技术

Q1 MULTIDISCIPLINARY SCIENCES

引用次数: 0

Abstract

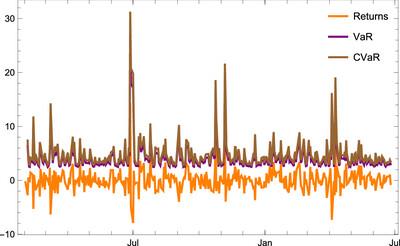

This paper introduces an approach to financial risk quantification by utilizing the Maxwell distribution as a foundation for deriving closed-form expressions of two essential risk measures: expected shortfall and value at risk. In contrast to classic solvers that predominantly depend on normality assumptions, the framework integrates these Maxwell-based formulations within a GARCH model structure, providing a theoretically grounded and computationally efficient alternative for risk assessment. The proposed methodology is empirically evaluated through forecasting on actual stock market data, demonstrating its practical effectiveness and robustness in capturing tail risk dynamics. This novelty stems from the fact that, unlike the Gaussian distribution, which systematically underestimates tail events due to its thin-tailed nature, the Maxwell distribution naturally accommodates heavier right tails and yields closed-form expressions for both VaR and ES. This provides a new analytical alternative for risk modeling beyond classical Gaussian-based frameworks.

关于获取经济风险的连续统计麦克斯韦分布

本文介绍了一种财务风险量化方法,利用麦克斯韦分布作为基础,推导出两个基本风险度量:预期不足和风险价值的封闭形式表达式。与主要依赖于正态性假设的经典求解器相比,该框架将这些基于麦克斯韦的公式集成到GARCH模型结构中,为风险评估提供了理论基础和计算效率高的替代方案。通过对实际股票市场数据的预测,实证验证了该方法在捕捉尾部风险动态方面的有效性和稳健性。这种新颖性源于这样一个事实,即与高斯分布不同,由于其细尾的性质,高斯分布系统地低估了尾部事件,麦克斯韦分布自然地容纳了较重的右尾,并产生了VaR和ES的封闭形式表达式。这为传统的基于高斯的框架之外的风险建模提供了一种新的分析选择。

本文章由计算机程序翻译,如有差异,请以英文原文为准。

求助全文

约1分钟内获得全文

求助全文

来源期刊

Advanced Theory and Simulations

Multidisciplinary-Multidisciplinary

CiteScore

5.50

自引率

3.00%

发文量

221

期刊介绍:

Advanced Theory and Simulations is an interdisciplinary, international, English-language journal that publishes high-quality scientific results focusing on the development and application of theoretical methods, modeling and simulation approaches in all natural science and medicine areas, including:

materials, chemistry, condensed matter physics

engineering, energy

life science, biology, medicine

atmospheric/environmental science, climate science

planetary science, astronomy, cosmology

method development, numerical methods, statistics

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: