{"title":"Modeling and Analysis of Trading Volume and Stock Return Data Using Bivariate q-Gaussian Distribution","authors":"T. Princy","doi":"10.1007/s40745-024-00578-5","DOIUrl":null,"url":null,"abstract":"<div><p>Two known characteristics of the distribution of stock returns (price fluctuations) and, more recently, the distribution of financial asset volumes are power laws and scaling. These power laws can be viewed as the asymptotic behaviour of distributions derived from nonextensive statistics, as demonstrated by an extensive number of instances in the field of physics. In this study, we explain the application of a non-extended statistics-based model for trading volume and stock price data. We present some novel theoretical results for the correlation between the trading volume distribution and stock return volatility that comes from entropy optimisation. We named this probability distribution as a bivariate <i>q</i>-Gaussian distribution since the resulting distribution is in terms of the <i>q</i>-exponential function, and when <i>q</i> tends to 1, it goes to the bivariate normal distribution. The primary characteristics of the novel model are thoroughly examined. The maximum likelihood estimation, a conventional technique, is used to conduct parameter estimation. The utility of the framing model is demonstrated using BSE Sensex data, which is used to illustrate the application of the bivariate <i>q</i>-Gaussian distribution.</p></div>","PeriodicalId":36280,"journal":{"name":"Annals of Data Science","volume":"12 5","pages":"1635 - 1659"},"PeriodicalIF":0.0000,"publicationDate":"2024-10-23","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Annals of Data Science","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s40745-024-00578-5","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"Decision Sciences","Score":null,"Total":0}

引用次数: 0

Abstract

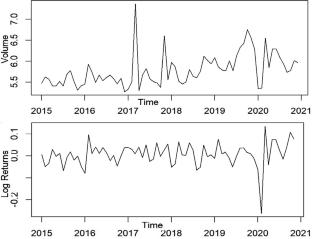

Two known characteristics of the distribution of stock returns (price fluctuations) and, more recently, the distribution of financial asset volumes are power laws and scaling. These power laws can be viewed as the asymptotic behaviour of distributions derived from nonextensive statistics, as demonstrated by an extensive number of instances in the field of physics. In this study, we explain the application of a non-extended statistics-based model for trading volume and stock price data. We present some novel theoretical results for the correlation between the trading volume distribution and stock return volatility that comes from entropy optimisation. We named this probability distribution as a bivariate q-Gaussian distribution since the resulting distribution is in terms of the q-exponential function, and when q tends to 1, it goes to the bivariate normal distribution. The primary characteristics of the novel model are thoroughly examined. The maximum likelihood estimation, a conventional technique, is used to conduct parameter estimation. The utility of the framing model is demonstrated using BSE Sensex data, which is used to illustrate the application of the bivariate q-Gaussian distribution.

期刊介绍:

Annals of Data Science (ADS) publishes cutting-edge research findings, experimental results and case studies of data science. Although Data Science is regarded as an interdisciplinary field of using mathematics, statistics, databases, data mining, high-performance computing, knowledge management and virtualization to discover knowledge from Big Data, it should have its own scientific contents, such as axioms, laws and rules, which are fundamentally important for experts in different fields to explore their own interests from Big Data. ADS encourages contributors to address such challenging problems at this exchange platform. At present, how to discover knowledge from heterogeneous data under Big Data environment needs to be addressed. ADS is a series of volumes edited by either the editorial office or guest editors. Guest editors will be responsible for call-for-papers and the review process for high-quality contributions in their volumes.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: