Sally Casswell, Karl Parker, Steve Randerson, Taisia Huckle, Lathika Athauda, Aravind Banavaram, Sarah Callinan, Orfhlaith Campbell, Surasak Chaiyasong, Song Dearak, Laura Romero-Garcia, Gopalkrishna Gururaj, Romtawan Kalapat, Khem Karki, Thomas Karlsson, Mom Kong, Shiwei Liu, Norman Maldonado, Juan Felipe González-Mejía, Tim Naimi, Keitseope Nthomang, Opeyemi Oladunni, Kwame Owino, Juan Herrera-Palacio, Phasith Phatchana, Pranil Pradhan, Ingeborg Rossow, Gillian Shorter, Vanlounny Sibounheuang, Mindaugas Štelemėkas, Dao The Son, Kate Vallance, Wim van Dalen, Ashley Wettlaufer, Arianne Zamora

{"title":"Investigating Indicators to Assess and Support Alcohol Taxation Policy: Results From the International Alcohol Control (IAC) Study.","authors":"Sally Casswell, Karl Parker, Steve Randerson, Taisia Huckle, Lathika Athauda, Aravind Banavaram, Sarah Callinan, Orfhlaith Campbell, Surasak Chaiyasong, Song Dearak, Laura Romero-Garcia, Gopalkrishna Gururaj, Romtawan Kalapat, Khem Karki, Thomas Karlsson, Mom Kong, Shiwei Liu, Norman Maldonado, Juan Felipe González-Mejía, Tim Naimi, Keitseope Nthomang, Opeyemi Oladunni, Kwame Owino, Juan Herrera-Palacio, Phasith Phatchana, Pranil Pradhan, Ingeborg Rossow, Gillian Shorter, Vanlounny Sibounheuang, Mindaugas Štelemėkas, Dao The Son, Kate Vallance, Wim van Dalen, Ashley Wettlaufer, Arianne Zamora","doi":"10.34172/ijhpm.8551","DOIUrl":null,"url":null,"abstract":"<p><p>Alcohol taxation is a key policy to reduce consumption and alcohol harm but evidence on tax design and indicators to assess taxation policy are lacking. Tax design and two indicators: tax as a share of lowest retail price and affordability, were investigated in eight high-income and nine middle-income jurisdictions. Collaborators populated the International Alcohol Control (IAC) study online Alcohol Policy Tool, providing measures of tax design, tax rates; and typical lowest prices available for retail take-away alcohol. These data were used to calculate tax/share of retail price. Affordability of alcohol was assessed against gross national income (GNI) per capita. High-income jurisdictions had higher tax/share and higher affordability on average compared with middle-income jurisdictions. Over the sample as a whole there was no association between these two indicators of tax policy. The tax designs used also varied with high-income jurisdictions more likely to use specific excise tax reflecting potency and middle-income jurisdictions more likely to utilise ad valorem and specific volume based taxes and to use more than one method across a beverage. Increased alcohol taxation to reduce alcohol consumption and harm is established as a high impact policy and is believed to work by affecting affordability. However, less is known about the best taxation methods to reduce affordability or the best measures to monitor and compare alcohol taxation between countries and over time. In this sample of high- and middle-income jurisdictions tax/price share was not found to predict affordability, suggesting the need to further research indicators of alcohol affordability.</p>","PeriodicalId":14135,"journal":{"name":"International Journal of Health Policy and Management","volume":"14 ","pages":"8551"},"PeriodicalIF":5.1000,"publicationDate":"2025-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC12257199/pdf/","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Journal of Health Policy and Management","FirstCategoryId":"3","ListUrlMain":"https://doi.org/10.34172/ijhpm.8551","RegionNum":3,"RegionCategory":"医学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2025/3/30 0:00:00","PubModel":"Epub","JCR":"Q2","JCRName":"HEALTH CARE SCIENCES & SERVICES","Score":null,"Total":0}

引用次数: 0

Abstract

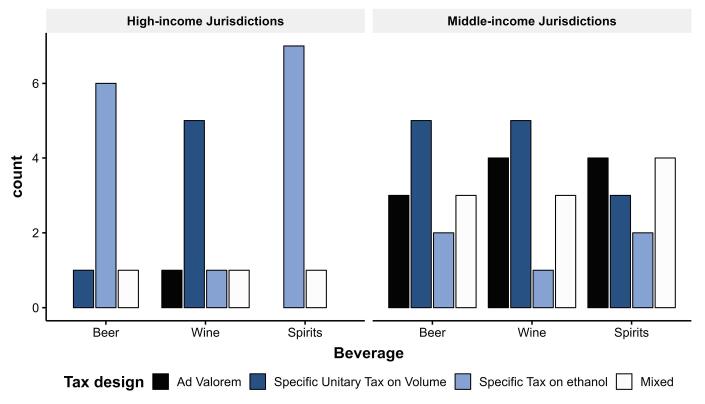

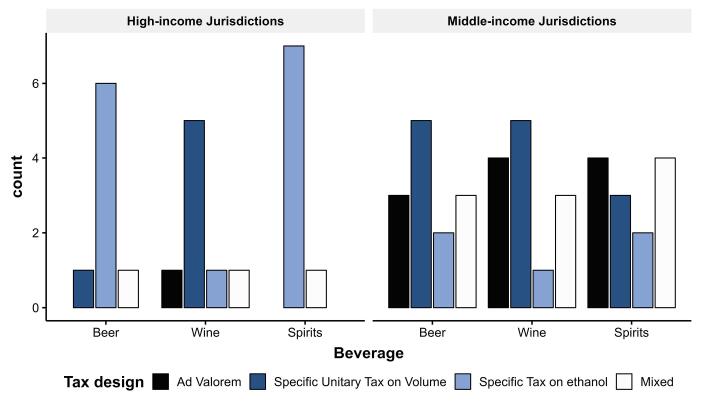

Alcohol taxation is a key policy to reduce consumption and alcohol harm but evidence on tax design and indicators to assess taxation policy are lacking. Tax design and two indicators: tax as a share of lowest retail price and affordability, were investigated in eight high-income and nine middle-income jurisdictions. Collaborators populated the International Alcohol Control (IAC) study online Alcohol Policy Tool, providing measures of tax design, tax rates; and typical lowest prices available for retail take-away alcohol. These data were used to calculate tax/share of retail price. Affordability of alcohol was assessed against gross national income (GNI) per capita. High-income jurisdictions had higher tax/share and higher affordability on average compared with middle-income jurisdictions. Over the sample as a whole there was no association between these two indicators of tax policy. The tax designs used also varied with high-income jurisdictions more likely to use specific excise tax reflecting potency and middle-income jurisdictions more likely to utilise ad valorem and specific volume based taxes and to use more than one method across a beverage. Increased alcohol taxation to reduce alcohol consumption and harm is established as a high impact policy and is believed to work by affecting affordability. However, less is known about the best taxation methods to reduce affordability or the best measures to monitor and compare alcohol taxation between countries and over time. In this sample of high- and middle-income jurisdictions tax/price share was not found to predict affordability, suggesting the need to further research indicators of alcohol affordability.

期刊介绍:

International Journal of Health Policy and Management (IJHPM) is a monthly open access, peer-reviewed journal which serves as an international and interdisciplinary setting for the dissemination of health policy and management research. It brings together individual specialties from different fields, notably health management/policy/economics, epidemiology, social/public policy, and philosophy into a dynamic academic mix.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: