{"title":"Sequential Monitoring for Changes in GARCH(1,1) Models Without Assuming Stationarity","authors":"Lajos Horváth, Lorenzo Trapani, Shixuan Wang","doi":"10.1111/jtsa.12824","DOIUrl":null,"url":null,"abstract":"<p>In this article, we develop two families of sequential monitoring procedure to (timely) detect changes in the parameters of a GARCH(1,1) model. Our statistics can be applied irrespective of whether the historical sample is stationary or not, and indeed without previous knowledge of the regime of the observations before and after the break. In particular, we construct our detectors as the CUSUM process of the quasi-Fisher scores of the log likelihood function. To ensure timely detection, we then construct our boundary function (exceeding which would indicate a break) by including a weighting sequence which is designed to shorten the detection delay in the presence of a changepoint. We consider two types of weights: a lighter set of weights, which ensures timely detection in the presence of changes occurring “early, but not too early” after the end of the historical sample; and a heavier set of weights, called “Rényi weights” which is designed to ensure timely detection in the presence of changepoints occurring very early in the monitoring horizon. In both cases, we derive the limiting distribution of the detection delays, indicating the expected delay for each set of weights. Our methodologies can be applied for a general analysis of changepoints in GARCH(1,1) sequences; however, they can also be applied to detect changes from stationarity to explosivity or vice versa, thus allowing to check for “volatility bubbles”, upon applying tests for stationarity before and after the identified break. Our theoretical results are validated via a comprehensive set of simulations, and an empirical application to daily returns of individual stocks.</p>","PeriodicalId":49973,"journal":{"name":"Journal of Time Series Analysis","volume":"46 5","pages":"981-996"},"PeriodicalIF":1.0000,"publicationDate":"2025-02-23","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jtsa.12824","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Time Series Analysis","FirstCategoryId":"100","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jtsa.12824","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS","Score":null,"Total":0}

引用次数: 0

Abstract

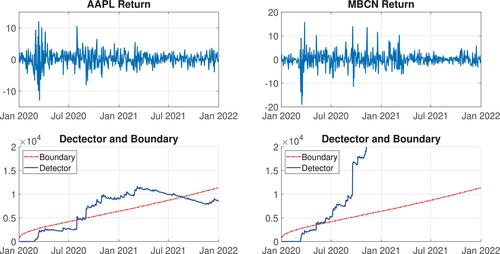

In this article, we develop two families of sequential monitoring procedure to (timely) detect changes in the parameters of a GARCH(1,1) model. Our statistics can be applied irrespective of whether the historical sample is stationary or not, and indeed without previous knowledge of the regime of the observations before and after the break. In particular, we construct our detectors as the CUSUM process of the quasi-Fisher scores of the log likelihood function. To ensure timely detection, we then construct our boundary function (exceeding which would indicate a break) by including a weighting sequence which is designed to shorten the detection delay in the presence of a changepoint. We consider two types of weights: a lighter set of weights, which ensures timely detection in the presence of changes occurring “early, but not too early” after the end of the historical sample; and a heavier set of weights, called “Rényi weights” which is designed to ensure timely detection in the presence of changepoints occurring very early in the monitoring horizon. In both cases, we derive the limiting distribution of the detection delays, indicating the expected delay for each set of weights. Our methodologies can be applied for a general analysis of changepoints in GARCH(1,1) sequences; however, they can also be applied to detect changes from stationarity to explosivity or vice versa, thus allowing to check for “volatility bubbles”, upon applying tests for stationarity before and after the identified break. Our theoretical results are validated via a comprehensive set of simulations, and an empirical application to daily returns of individual stocks.

期刊介绍:

During the last 30 years Time Series Analysis has become one of the most important and widely used branches of Mathematical Statistics. Its fields of application range from neurophysiology to astrophysics and it covers such well-known areas as economic forecasting, study of biological data, control systems, signal processing and communications and vibrations engineering.

The Journal of Time Series Analysis started in 1980, has since become the leading journal in its field, publishing papers on both fundamental theory and applications, as well as review papers dealing with recent advances in major areas of the subject and short communications on theoretical developments. The editorial board consists of many of the world''s leading experts in Time Series Analysis.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: