{"title":"Multiple Seasonal Autoregressive Integrated Moving Average Models","authors":"Francesco Lisi, Matteo Grigoletto","doi":"10.1002/for.3283","DOIUrl":null,"url":null,"abstract":"<p>Many empirical time series show periodic patterns. SARIMA models and exponential smoothing methods are classical approaches to account for seasonal dynamics. However, they allow to model just one periodic component, while several time series have multiple seasonality, with periodic components possibly tangled among them. To face this case, some seasonal-trend decomposition methods have been proposed in the literature, for example, the TBATS model, the MSTL model, the ADAM model, and the Prophet model, while SARIMA models have been quite neglected. To fill this gap, in this work, we suggest a suitable generalization of the SARIMA model, called mSARIMA, able to account for multiple seasonality. First, we define the model, describe its characteristics, and propose a test for residual multiperiodic correlation. Then, we analyze the predictive performance by comparing the mSARIMA model with other approaches, namely, the TBATS, MSTL, ADAM, and Prophet models, under different kinds of seasonality. The results suggest that when seasonality has a stochastic nature, mSARIMA models are more effective in predicting the series. However, if seasonality is basically deterministic, then the model decomposition approach is more suitable. Finally, we provide two comparative forecasting applications for the 5-min series of the number of calls handled by a large North American commercial bank and for the 10-min traffic data on the eastbound lanes of the Ventura Highway in Los Angeles.</p>","PeriodicalId":47835,"journal":{"name":"Journal of Forecasting","volume":"44 6","pages":"2037-2052"},"PeriodicalIF":2.7000,"publicationDate":"2025-05-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/for.3283","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Forecasting","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/for.3283","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

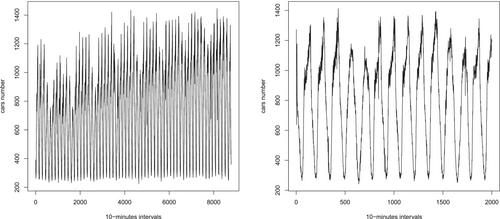

Many empirical time series show periodic patterns. SARIMA models and exponential smoothing methods are classical approaches to account for seasonal dynamics. However, they allow to model just one periodic component, while several time series have multiple seasonality, with periodic components possibly tangled among them. To face this case, some seasonal-trend decomposition methods have been proposed in the literature, for example, the TBATS model, the MSTL model, the ADAM model, and the Prophet model, while SARIMA models have been quite neglected. To fill this gap, in this work, we suggest a suitable generalization of the SARIMA model, called mSARIMA, able to account for multiple seasonality. First, we define the model, describe its characteristics, and propose a test for residual multiperiodic correlation. Then, we analyze the predictive performance by comparing the mSARIMA model with other approaches, namely, the TBATS, MSTL, ADAM, and Prophet models, under different kinds of seasonality. The results suggest that when seasonality has a stochastic nature, mSARIMA models are more effective in predicting the series. However, if seasonality is basically deterministic, then the model decomposition approach is more suitable. Finally, we provide two comparative forecasting applications for the 5-min series of the number of calls handled by a large North American commercial bank and for the 10-min traffic data on the eastbound lanes of the Ventura Highway in Los Angeles.

期刊介绍:

The Journal of Forecasting is an international journal that publishes refereed papers on forecasting. It is multidisciplinary, welcoming papers dealing with any aspect of forecasting: theoretical, practical, computational and methodological. A broad interpretation of the topic is taken with approaches from various subject areas, such as statistics, economics, psychology, systems engineering and social sciences, all encouraged. Furthermore, the Journal welcomes a wide diversity of applications in such fields as business, government, technology and the environment. Of particular interest are papers dealing with modelling issues and the relationship of forecasting systems to decision-making processes.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: