{"title":"Measuring the Impact of Transition Risk on Financial Markets: A Joint VaR-ES Approach","authors":"Laura Garcia-Jorcano, Lidia Sanchis-Marco","doi":"10.1002/for.3274","DOIUrl":null,"url":null,"abstract":"<p>Based on a joint quantile and expected shortfall semiparametric methodology, we propose a novel approach to forecasting market risk conditioned to transition risk exposure. This method allows us to forecast two climate-related financial risk measures called \n<span></span><math>\n <mi>C</mi>\n <mi>o</mi>\n <mi>C</mi>\n <mi>l</mi>\n <mi>i</mi>\n <mi>m</mi>\n <mi>a</mi>\n <mi>t</mi>\n <mi>e</mi>\n <mi>V</mi>\n <mi>a</mi>\n <mi>R</mi></math> and \n<span></span><math>\n <mi>C</mi>\n <mi>o</mi>\n <mi>C</mi>\n <mi>l</mi>\n <mi>i</mi>\n <mi>m</mi>\n <mi>a</mi>\n <mi>t</mi>\n <mi>e</mi>\n <mi>E</mi>\n <mi>S</mi></math>, being jointly elicitable, that capture the dependence of the European extreme bank returns on changes in carbon returns at extreme quantiles representing green and brown states. We evaluate our approach using a novel backtesting procedure and introduce related measures (\n<span></span><math>\n <mi>Δ</mi>\n <mi>C</mi>\n <mi>o</mi>\n <mi>C</mi>\n <mi>l</mi>\n <mi>i</mi>\n <mi>m</mi>\n <mi>a</mi>\n <mi>t</mi>\n <mi>e</mi></math> and \n<span></span><math>\n <mi>E</mi>\n <mi>x</mi>\n <mi>p</mi>\n <mi>o</mi>\n <mi>s</mi>\n <mi>u</mi>\n <mi>r</mi>\n <mi>e</mi>\n <mi>C</mi>\n <mi>l</mi>\n <mi>i</mi>\n <mi>m</mi>\n <mi>a</mi>\n <mi>t</mi>\n <mi>e</mi></math>). The main evidence states that the \n<span></span><math>\n <mi>C</mi>\n <mi>o</mi>\n <mi>C</mi>\n <mi>l</mi>\n <mi>i</mi>\n <mi>m</mi>\n <mi>a</mi>\n <mi>t</mi>\n <mi>e</mi>\n <mi>E</mi>\n <mi>S</mi></math> measure presents the highest risk for the brown (green) state due to the presence of carbon cost (carbon risk premium) in Ph.II (Ph.III) of the EU Emissions Trading System. Furthermore, we found the highest (lowest) financial risk forecasts for \n<span></span><math>\n <mi>C</mi>\n <mi>o</mi>\n <mi>C</mi>\n <mi>l</mi>\n <mi>i</mi>\n <mi>m</mi>\n <mi>a</mi>\n <mi>t</mi>\n <mi>e</mi>\n <mi>E</mi>\n <mi>S</mi></math> in green (brown) states during COVID-19. These results offer important implications for investors and policymakers regarding the effects of transition risk on the European financial system.</p>","PeriodicalId":47835,"journal":{"name":"Journal of Forecasting","volume":"44 6","pages":"1907-1945"},"PeriodicalIF":2.7000,"publicationDate":"2025-04-09","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/for.3274","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Forecasting","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/for.3274","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

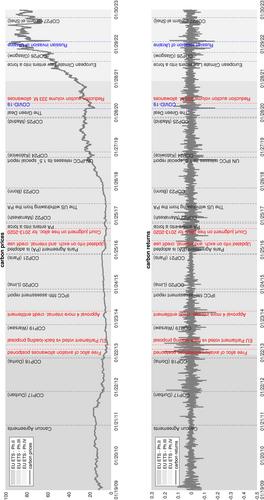

Abstract

Based on a joint quantile and expected shortfall semiparametric methodology, we propose a novel approach to forecasting market risk conditioned to transition risk exposure. This method allows us to forecast two climate-related financial risk measures called

and

, being jointly elicitable, that capture the dependence of the European extreme bank returns on changes in carbon returns at extreme quantiles representing green and brown states. We evaluate our approach using a novel backtesting procedure and introduce related measures (

and

). The main evidence states that the

measure presents the highest risk for the brown (green) state due to the presence of carbon cost (carbon risk premium) in Ph.II (Ph.III) of the EU Emissions Trading System. Furthermore, we found the highest (lowest) financial risk forecasts for

in green (brown) states during COVID-19. These results offer important implications for investors and policymakers regarding the effects of transition risk on the European financial system.

基于联合分位数和预期不足半参数方法,提出了一种以过渡风险暴露为条件的市场风险预测方法。这种方法使我们能够预测两种与气候相关的金融风险指标,即C / C / C / C / R和C / C / C / C / C / S,它们是共同可获得的。捕捉了欧洲极端银行回报对代表绿色和棕色州的极端分位数的碳回报变化的依赖。我们评估我们的方法使用一个小说,val过程和采取相关措施 ( Δ C o C l 我 米 一个 t e和 E x p o 年代 u r e C l 我 米 一个 t e)。主要证据表明,由于欧盟排放交易体系Ph.II (Ph.III)中的碳成本(碳风险溢价)的存在,碳/碳/碳排放在e / S测量中对棕色(绿色)州的风险最高。此外,我们发现,在2019冠状病毒病期间,绿色(棕色)州的最高(最低)金融风险预测为美国和美国。这些结果为投资者和政策制定者提供了关于转型风险对欧洲金融体系影响的重要启示。

期刊介绍:

The Journal of Forecasting is an international journal that publishes refereed papers on forecasting. It is multidisciplinary, welcoming papers dealing with any aspect of forecasting: theoretical, practical, computational and methodological. A broad interpretation of the topic is taken with approaches from various subject areas, such as statistics, economics, psychology, systems engineering and social sciences, all encouraged. Furthermore, the Journal welcomes a wide diversity of applications in such fields as business, government, technology and the environment. Of particular interest are papers dealing with modelling issues and the relationship of forecasting systems to decision-making processes.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: