{"title":"A multi-stage machine learning approach for stock price prediction: Engineered and derivative indices","authors":"Shaghayegh Abolmakarem , Farshid Abdi , Kaveh Khalili-Damghani , Hosein Didehkhani","doi":"10.1016/j.iswa.2024.200449","DOIUrl":null,"url":null,"abstract":"<div><div>In this paper, a machine learning approach is proposed to predict the next day's stock prices. The methodology involves comprehensive data collection and feature generation, followed by predictions utilizing Multi-Layer Perceptron (MLP) networks. We selected 5,283 records of daily historical data, including open prices, close prices, highest prices, lowest prices, and trading volumes from four well-known stocks in the FTSE 100 index. A novel set of engineered and derivative indices is extracted from the original time series to enhance prediction accuracy. Two Multi-Layer Perceptron (MLP) are proposed to predict the next day's stock prices using the engineered discrete and continuous indices. The case study uses the daily historical time series of stock prices between January 1, 2000, and December 31, 2020. The proposed machine learning approach presents suitable applicability and accuracy, respectively.</div></div>","PeriodicalId":100684,"journal":{"name":"Intelligent Systems with Applications","volume":"24 ","pages":"Article 200449"},"PeriodicalIF":4.3000,"publicationDate":"2024-10-06","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Intelligent Systems with Applications","FirstCategoryId":"1085","ListUrlMain":"https://www.sciencedirect.com/science/article/pii/S2667305324001236","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

引用次数: 0

Abstract

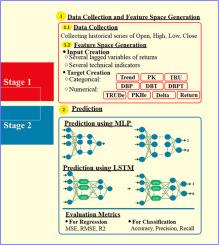

In this paper, a machine learning approach is proposed to predict the next day's stock prices. The methodology involves comprehensive data collection and feature generation, followed by predictions utilizing Multi-Layer Perceptron (MLP) networks. We selected 5,283 records of daily historical data, including open prices, close prices, highest prices, lowest prices, and trading volumes from four well-known stocks in the FTSE 100 index. A novel set of engineered and derivative indices is extracted from the original time series to enhance prediction accuracy. Two Multi-Layer Perceptron (MLP) are proposed to predict the next day's stock prices using the engineered discrete and continuous indices. The case study uses the daily historical time series of stock prices between January 1, 2000, and December 31, 2020. The proposed machine learning approach presents suitable applicability and accuracy, respectively.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: