{"title":"Enhancing financial time series forecasting in the shipping market: A hybrid approach with Light Gradient Boosting Machine","authors":"Xuefei Song , Zhong Shuo Chen","doi":"10.1016/j.engappai.2024.108942","DOIUrl":null,"url":null,"abstract":"<div><p>Accurately forecasting financial time series in the dynamic shipping market is vital for stakeholders, such as shipowners, investors, brokers, and shipyards. This paper introduces an innovative hybrid machine learning model leveraging Light Gradient Boosting Machine (LightGBM) to enhance financial time series predictions within the international shipping sector. LightGBM, known for its efficiency and scalability in handling high-dimensional data, offers a robust foundation for this forecasting endeavor. However, LightGBM fails to extract temporal features from time series data. Time series usually contain multi-scale information with different frequencies, but LightGBM directly learns from the original time series, and the forecasting accuracy is unsatisfactory. To address this challenge, we propose a two-stage hybrid forecasting model. In the initial stage, we employ the variational mode decomposition method to extract predictive features from the time series data online. Subsequently, we employ LightGBM for forecasting purposes, capitalizing on its superior capabilities. To validate the effectiveness of our approach, we conduct an extensive empirical study involving sixteen distinct time series from the global shipping market. We illustrate the model’s superiority in forecasting accuracy and reliability through comprehensive comparisons with state-of-the-art methods from the existing literature. This research provides valuable insights for stakeholders and showcases the potential of hybrid machine learning techniques for financial time series forecasting in complex and dynamic markets.</p></div>","PeriodicalId":50523,"journal":{"name":"Engineering Applications of Artificial Intelligence","volume":"136 ","pages":"Article 108942"},"PeriodicalIF":7.5000,"publicationDate":"2024-07-15","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Engineering Applications of Artificial Intelligence","FirstCategoryId":"94","ListUrlMain":"https://www.sciencedirect.com/science/article/pii/S095219762401100X","RegionNum":2,"RegionCategory":"计算机科学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"AUTOMATION & CONTROL SYSTEMS","Score":null,"Total":0}

引用次数: 0

Abstract

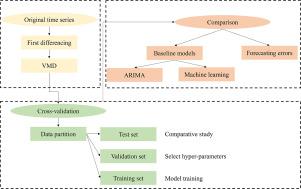

Accurately forecasting financial time series in the dynamic shipping market is vital for stakeholders, such as shipowners, investors, brokers, and shipyards. This paper introduces an innovative hybrid machine learning model leveraging Light Gradient Boosting Machine (LightGBM) to enhance financial time series predictions within the international shipping sector. LightGBM, known for its efficiency and scalability in handling high-dimensional data, offers a robust foundation for this forecasting endeavor. However, LightGBM fails to extract temporal features from time series data. Time series usually contain multi-scale information with different frequencies, but LightGBM directly learns from the original time series, and the forecasting accuracy is unsatisfactory. To address this challenge, we propose a two-stage hybrid forecasting model. In the initial stage, we employ the variational mode decomposition method to extract predictive features from the time series data online. Subsequently, we employ LightGBM for forecasting purposes, capitalizing on its superior capabilities. To validate the effectiveness of our approach, we conduct an extensive empirical study involving sixteen distinct time series from the global shipping market. We illustrate the model’s superiority in forecasting accuracy and reliability through comprehensive comparisons with state-of-the-art methods from the existing literature. This research provides valuable insights for stakeholders and showcases the potential of hybrid machine learning techniques for financial time series forecasting in complex and dynamic markets.

期刊介绍:

Artificial Intelligence (AI) is pivotal in driving the fourth industrial revolution, witnessing remarkable advancements across various machine learning methodologies. AI techniques have become indispensable tools for practicing engineers, enabling them to tackle previously insurmountable challenges. Engineering Applications of Artificial Intelligence serves as a global platform for the swift dissemination of research elucidating the practical application of AI methods across all engineering disciplines. Submitted papers are expected to present novel aspects of AI utilized in real-world engineering applications, validated using publicly available datasets to ensure the replicability of research outcomes. Join us in exploring the transformative potential of AI in engineering.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: