Thi Minh Huong Le, Thi Nga My Nguyen, Thi Yen Vinh Tran

{"title":"Spillover Effects of Oil Price Fluctuations on the U.S and Asia–Pacific Stock Markets: A Multivariate EGARCH Analysis","authors":"Thi Minh Huong Le, Thi Nga My Nguyen, Thi Yen Vinh Tran","doi":"10.1007/s10690-024-09480-9","DOIUrl":null,"url":null,"abstract":"<div><p>This study investigates the spillover effects between oil and stock prices from 2000 to 2022, utilizing the multivariate EGARCH model. The database includes three periods—the entire sample, the pre-pandemic era, and COVID-19. The analysis unveils insights into the dynamics of spillover effects. Findings reveal an asymmetry in spillover effects, with a prevailing negative impact trend from oil to stocks, notably affecting the Thai index negatively while positively impacting the Indonesian market. Considering the entire time frame, results address the dynamic spillover effects of oil on eight stock indices across 11 countries under analysis. Meanwhile, in the absence of a pandemic, there are only mutual relationships between oil and stock markets in five stock markets. During COVID-19, we witnessed an intensified spillover effect from oil prices to stocks, with only the Vietnamese stock market remaining unaffected. Notably, the overall spillover level peaked at 55% in 2018, decreasing to over 45% during the COVID-19 pandemic, indicating a close relationship between oil and stocks. Additional results confirm the stationarity of return data series and support the application of the multivariate EGARCH model, enhancing the study’s robustness and contributing to understanding the intricate dynamics of financial markets.</p></div>","PeriodicalId":54095,"journal":{"name":"Asia-Pacific Financial Markets","volume":"32 3","pages":"1049 - 1076"},"PeriodicalIF":2.6000,"publicationDate":"2024-07-03","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Asia-Pacific Financial Markets","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s10690-024-09480-9","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

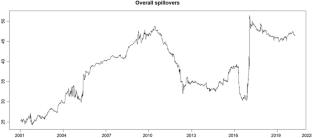

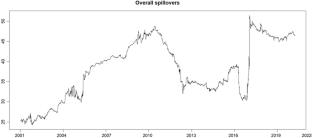

This study investigates the spillover effects between oil and stock prices from 2000 to 2022, utilizing the multivariate EGARCH model. The database includes three periods—the entire sample, the pre-pandemic era, and COVID-19. The analysis unveils insights into the dynamics of spillover effects. Findings reveal an asymmetry in spillover effects, with a prevailing negative impact trend from oil to stocks, notably affecting the Thai index negatively while positively impacting the Indonesian market. Considering the entire time frame, results address the dynamic spillover effects of oil on eight stock indices across 11 countries under analysis. Meanwhile, in the absence of a pandemic, there are only mutual relationships between oil and stock markets in five stock markets. During COVID-19, we witnessed an intensified spillover effect from oil prices to stocks, with only the Vietnamese stock market remaining unaffected. Notably, the overall spillover level peaked at 55% in 2018, decreasing to over 45% during the COVID-19 pandemic, indicating a close relationship between oil and stocks. Additional results confirm the stationarity of return data series and support the application of the multivariate EGARCH model, enhancing the study’s robustness and contributing to understanding the intricate dynamics of financial markets.

期刊介绍:

The current remarkable growth in the Asia-Pacific financial markets is certain to continue. These markets are expected to play a further important role in the world capital markets for investment and risk management. In accordance with this development, Asia-Pacific Financial Markets (formerly Financial Engineering and the Japanese Markets), the official journal of the Japanese Association of Financial Econometrics and Engineering (JAFEE), is expected to provide an international forum for researchers and practitioners in academia, industry, and government, who engage in empirical and/or theoretical research into the financial markets. We invite submission of quality papers on all aspects of finance and financial engineering.

Here we interpret the term ''financial engineering'' broadly enough to cover such topics as financial time series, portfolio analysis, global asset allocation, trading strategy for investment, optimization methods, macro monetary economic analysis and pricing models for various financial assets including derivatives We stress that purely theoretical papers, as well as empirical studies that use Asia-Pacific market data, are welcome.

Officially cited as: Asia-Pac Financ Markets

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: