{"title":"A New Index of Option Implied Absolute Deviation","authors":"George Dotsis","doi":"10.1002/fut.22537","DOIUrl":null,"url":null,"abstract":"<p>This paper proposes a new index of forward looking absolute deviation extracted from option prices. The new index, named absolute deviation index (ADIX), is model-free and easy to compute using at-the-money call and put option prices. It is shown that the spread between volatility index (VIX) and ADIX captures departures from normality in the risk-neutral distribution and an empirical analysis using S&P 500 options data for the time period 1996–2021 reveals that the spread carries significant forecasting ability with respect to future equity returns at short to medium horizons. Portfolio strategies that use the spread as a predictor of S&P 500 returns outperform buy-and-hold strategies in an out-of-sample mean-variance asset allocation exercise.</p>","PeriodicalId":15863,"journal":{"name":"Journal of Futures Markets","volume":"44 9","pages":"1543-1555"},"PeriodicalIF":2.3000,"publicationDate":"2024-07-04","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/fut.22537","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Futures Markets","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/fut.22537","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

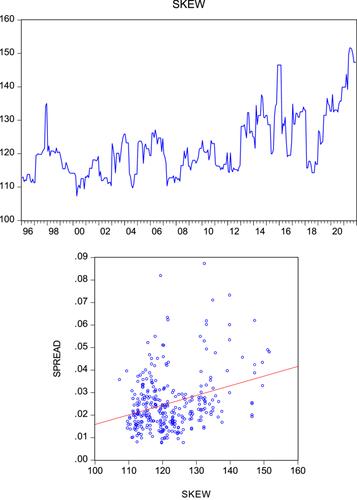

Abstract

This paper proposes a new index of forward looking absolute deviation extracted from option prices. The new index, named absolute deviation index (ADIX), is model-free and easy to compute using at-the-money call and put option prices. It is shown that the spread between volatility index (VIX) and ADIX captures departures from normality in the risk-neutral distribution and an empirical analysis using S&P 500 options data for the time period 1996–2021 reveals that the spread carries significant forecasting ability with respect to future equity returns at short to medium horizons. Portfolio strategies that use the spread as a predictor of S&P 500 returns outperform buy-and-hold strategies in an out-of-sample mean-variance asset allocation exercise.

期刊介绍:

The Journal of Futures Markets chronicles the latest developments in financial futures and derivatives. It publishes timely, innovative articles written by leading finance academics and professionals. Coverage ranges from the highly practical to theoretical topics that include futures, derivatives, risk management and control, financial engineering, new financial instruments, hedging strategies, analysis of trading systems, legal, accounting, and regulatory issues, and portfolio optimization. This publication contains the very latest research from the top experts.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: