Forecasting Bitcoin returns: Econometric time series analysis vs. machine learning

IF 3.4

3区 经济学

Q1 ECONOMICS

引用次数: 0

Abstract

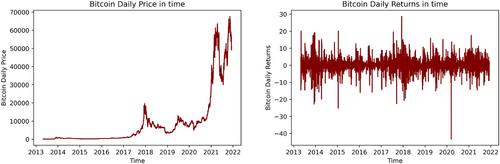

We study the statistical properties of the Bitcoin return series and provide a thorough forecasting exercise. Also, we calibrate state-of-the-art machine learning techniques and compare the results with econometric time series models. The empirical assessment provides evidence that the application of machine learning techniques outperforms econometric benchmarks in terms of forecasting precision for both in- and out-of-sample forecasts. We find that both deep learning architectures as well as complex layers, such as LSTM, do not increase the precision of daily forecasts. Specifically, a simple recurrent neural network describes a sensible choice for forecasting daily return series.

预测比特币收益:计量经济学时间序列分析与机器学习

我们研究了比特币回报序列的统计特性,并提供了全面的预测练习。此外,我们还校准了最先进的机器学习技术,并将结果与计量经济学时间序列模型进行了比较。实证评估提供的证据表明,在样本内和样本外预测方面,机器学习技术的应用在预测精度上优于计量经济学基准。我们发现,深度学习架构和复杂层(如 LSTM)都无法提高每日预测的精度。具体来说,简单的递归神经网络是预测每日回报序列的明智选择。

本文章由计算机程序翻译,如有差异,请以英文原文为准。

求助全文

约1分钟内获得全文

求助全文

来源期刊

Journal of Forecasting

Multiple-

CiteScore

5.40

自引率

5.90%

发文量

91

期刊介绍:

The Journal of Forecasting is an international journal that publishes refereed papers on forecasting. It is multidisciplinary, welcoming papers dealing with any aspect of forecasting: theoretical, practical, computational and methodological. A broad interpretation of the topic is taken with approaches from various subject areas, such as statistics, economics, psychology, systems engineering and social sciences, all encouraged. Furthermore, the Journal welcomes a wide diversity of applications in such fields as business, government, technology and the environment. Of particular interest are papers dealing with modelling issues and the relationship of forecasting systems to decision-making processes.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: