{"title":"Forecasting and Analyzing Predictors of Inflation Rate: Using Machine Learning Approach","authors":"Pijush Kanti Das, Prabir Kumar Das","doi":"10.1007/s40953-024-00384-z","DOIUrl":null,"url":null,"abstract":"<p>In this study, we investigate and apply the models from the machine learning (ML) paradigm to forecast the inflation rate. The models identified are ridge, lasso, elastic net, random forest, and artificial neural network. We carry out the analysis using a data set with 56 features of 132 monthly observations from January 2012 to December 2022. The random forest (RF) model can forecast the inflation rate with greater accuracy than other ML models. A comparison to benchmark econometric models like auto-regressive integrated moving average demonstrates the superior performance of the RF model. Moreover, nonlinear ML models are proven to be more successful than a linear ML or time series models and this is mostly due to the unpredictability and interactions of variables. It indicates that the significance of nonlinear structures for forecasting inflation is important. Furthermore, the ML models outweigh the benchmark econometric model in forecasting the undulations due to the COVID-19 impact. The findings in this study support the benefit of applying ML models to forecast the inflation rate. Even without considering the sporadicity of pandemic, nonlinear model like artificial neural network (ANN) outweighs other models. Additionally, the ML models like RF and ANN model yield variable importance measures for each explanatory variable. ML models shows capability to not only better forecasting but also able to provide the insight regarding the covariates for improved forecasting results and policy prescriptions.</p>","PeriodicalId":42219,"journal":{"name":"JOURNAL OF QUANTITATIVE ECONOMICS","volume":"51 1","pages":""},"PeriodicalIF":0.6000,"publicationDate":"2024-02-29","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"JOURNAL OF QUANTITATIVE ECONOMICS","FirstCategoryId":"91","ListUrlMain":"https://doi.org/10.1007/s40953-024-00384-z","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

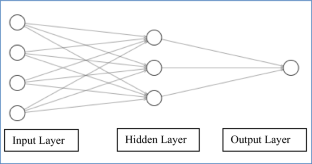

Abstract

In this study, we investigate and apply the models from the machine learning (ML) paradigm to forecast the inflation rate. The models identified are ridge, lasso, elastic net, random forest, and artificial neural network. We carry out the analysis using a data set with 56 features of 132 monthly observations from January 2012 to December 2022. The random forest (RF) model can forecast the inflation rate with greater accuracy than other ML models. A comparison to benchmark econometric models like auto-regressive integrated moving average demonstrates the superior performance of the RF model. Moreover, nonlinear ML models are proven to be more successful than a linear ML or time series models and this is mostly due to the unpredictability and interactions of variables. It indicates that the significance of nonlinear structures for forecasting inflation is important. Furthermore, the ML models outweigh the benchmark econometric model in forecasting the undulations due to the COVID-19 impact. The findings in this study support the benefit of applying ML models to forecast the inflation rate. Even without considering the sporadicity of pandemic, nonlinear model like artificial neural network (ANN) outweighs other models. Additionally, the ML models like RF and ANN model yield variable importance measures for each explanatory variable. ML models shows capability to not only better forecasting but also able to provide the insight regarding the covariates for improved forecasting results and policy prescriptions.

期刊介绍:

The Journal of Quantitative Economics (JQEC) is a refereed journal of the Indian Econometric Society (TIES). It solicits quantitative papers with basic or applied research orientation in all sub-fields of Economics that employ rigorous theoretical, empirical and experimental methods. The Journal also encourages Short Papers and Review Articles. Innovative and fundamental papers that focus on various facets of Economics of the Emerging Market and Developing Economies are particularly welcome. With the help of an international Editorial board and carefully selected referees, it aims to minimize the time taken to complete the review process while preserving the quality of the articles published.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: