Spillover in higher-order moments across carbon and energy markets: A portfolio view

IF 3.1

3区 经济学

Q2 BUSINESS, FINANCE

引用次数: 0

Abstract

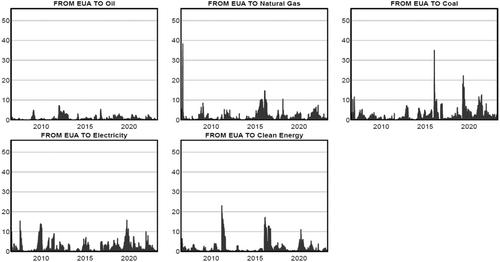

Motivated by the occurrence of extreme events and nonnormality of returns, we examine the spillovers among the conditional volatility, skewness and (excess) kurtosis of European Union allowances (EUA), Brent oil, natural gas, coal, electricity and clean energy markets. The jointly estimated spillover index in the system of the three higher-order moments is notably high, exceeding the spillover index estimated for each individual moment separately. This suggests that spillovers across moments in the carbon-energy system are important for the sake of completeness of the spillover analysis, and should not be ignored. The performance of the portfolio improves after considering higher-order moments.

碳和能源市场高阶矩的溢出效应:组合观点

受极端事件的发生和收益率非正态性的影响,我们研究了欧盟配额(EUA)、布伦特石油、天然气、煤炭、电力和清洁能源市场的条件波动率、偏度和(超)峰度之间的溢出效应。在三个高阶矩的系统中,联合估算的溢出指数明显较高,超过了对每个单独矩的溢出指数估算。这表明,碳-能源系统中不同时刻的溢出效应对于溢出效应分析的完整性非常重要,不应被忽视。考虑高阶时刻后,投资组合的绩效有所改善。

本文章由计算机程序翻译,如有差异,请以英文原文为准。

求助全文

约1分钟内获得全文

求助全文

来源期刊

European Financial Management

BUSINESS, FINANCE-

CiteScore

4.30

自引率

18.20%

发文量

60

期刊介绍:

European Financial Management publishes the best research from around the world, providing a forum for both academics and practitioners concerned with the financial management of modern corporation and financial institutions. The journal publishes signficant new finance research on timely issues and highlights key trends in Europe in a clear and accessible way, with articles covering international research and practice that have direct or indirect bearing on Europe.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: