The pass-through of temporary VAT rate cuts: evidence from German supermarket retail

IF 1.4

4区 经济学

Q3 ECONOMICS

引用次数: 0

Abstract

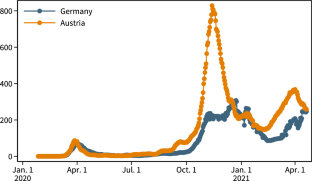

We study the price effects of a temporary VAT reduction in Germany using a web-scraped dataset of daily prices of more than 60000 supermarket products. For causal identification, we compare the development of German prices to those in Austria. We find that the reduction of VAT rates led to a price decrease of 1.3%, implying that 70% of the tax cut were passed on to consumers. Moreover, the pass-through is higher for vertically integrated products (private label) than for independent brands. This is consistent with menu cost theories and theories predicting that price markups act as a buffer for cost shocks.

临时性增值税税率下调的传递:来自德国超市零售业的证据

我们使用网络抓取的 60000 多种超市产品的每日价格数据集,研究了德国临时降低增值税对价格的影响。为了确定因果关系,我们将德国与奥地利的价格发展情况进行了比较。我们发现,增值税税率的降低导致价格下降了 1.3%,这意味着 70% 的减税被转嫁给了消费者。此外,垂直整合产品(自有品牌)的转嫁率高于独立品牌。这与菜单成本理论和价格加价对成本冲击起到缓冲作用的理论预测是一致的。

本文章由计算机程序翻译,如有差异,请以英文原文为准。

求助全文

约1分钟内获得全文

求助全文

来源期刊

International Tax and Public Finance

ECONOMICS-

CiteScore

2.40

自引率

10.00%

发文量

56

期刊介绍:

INTERNATIONAL TAX AND PUBLIC FINANCE publishes outstanding original research, both theoretical and empirical, in all areas of public economics. While the journal has a historical strength in open economy, international, and interjurisdictional issues, we actively encourage high-quality submissions from the breadth of public economics.The special Policy Watch section is designed to facilitate communication between the academic and public policy spheres. This section includes timely, policy-oriented discussions. The goal is to provide a two-way forum in which academic researchers gain insight into current policy priorities and policy-makers can access academic advances in a practical way. INTERNATIONAL TAX AND PUBLIC FINANCE is peer reviewed and published in one volume per year, consisting of six issues, one of which contains papers presented at the annual congress of the International Institute of Public Finance (refereed in the usual way). Officially cited as: Int Tax Public Finance

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: