{"title":"Rewarding good taxpayers: an effective mechanism?","authors":"Pedro A. Cabra-Acela","doi":"10.1007/s10797-022-09771-9","DOIUrl":null,"url":null,"abstract":"<p>This paper studies the conditions under which rewarding compliant taxpayers is an optimal mechanism to improve tax collection. The theoretical model suggests that when auditing contributors and evading are both costly, rewarding tax compliance is an effective strategy to increase the government’s profit. I provide empirical evidence from the Argentinian provinces’ rewards and tax policy variation. Where the data suggest that theoretical conditions hold, there is a positive effect in the real estate per-capita tax collection ranging from 0.4 to more than 2 standard deviations. This result has important policy implications, mapping the private evasion cost and the price of traditional policy tools as the main determinants of positive incentives’ effectiveness.</p>","PeriodicalId":47518,"journal":{"name":"International Tax and Public Finance","volume":"40 4","pages":""},"PeriodicalIF":1.4000,"publicationDate":"2022-12-06","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Tax and Public Finance","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s10797-022-09771-9","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

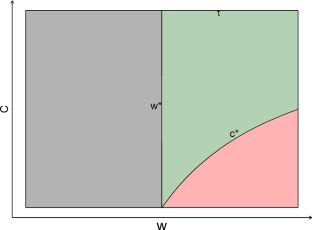

This paper studies the conditions under which rewarding compliant taxpayers is an optimal mechanism to improve tax collection. The theoretical model suggests that when auditing contributors and evading are both costly, rewarding tax compliance is an effective strategy to increase the government’s profit. I provide empirical evidence from the Argentinian provinces’ rewards and tax policy variation. Where the data suggest that theoretical conditions hold, there is a positive effect in the real estate per-capita tax collection ranging from 0.4 to more than 2 standard deviations. This result has important policy implications, mapping the private evasion cost and the price of traditional policy tools as the main determinants of positive incentives’ effectiveness.

期刊介绍:

INTERNATIONAL TAX AND PUBLIC FINANCE publishes outstanding original research, both theoretical and empirical, in all areas of public economics. While the journal has a historical strength in open economy, international, and interjurisdictional issues, we actively encourage high-quality submissions from the breadth of public economics.The special Policy Watch section is designed to facilitate communication between the academic and public policy spheres. This section includes timely, policy-oriented discussions. The goal is to provide a two-way forum in which academic researchers gain insight into current policy priorities and policy-makers can access academic advances in a practical way. INTERNATIONAL TAX AND PUBLIC FINANCE is peer reviewed and published in one volume per year, consisting of six issues, one of which contains papers presented at the annual congress of the International Institute of Public Finance (refereed in the usual way). Officially cited as: Int Tax Public Finance

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: