Round number reference points and irregular patterns in reported gross margins

IF 5.8

3区 管理学

Q1 BUSINESS, FINANCE

引用次数: 0

Abstract

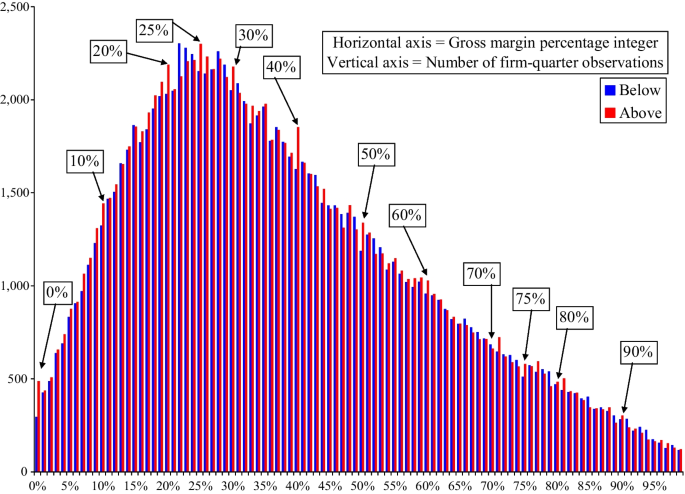

Abstract We find irregular patterns in the distribution of firms’ reported quarterly gross margin percentages. Specifically, there is significant bunching around percentage integers that are highly round (e.g., multiples of 10, such as 30%, 40%, etc.) or are neatly divisible (e.g., 25%, 75%), compared to what is predicted by counterfactual distributions. Further investigation reveals that highly round gross margin firms are smaller, exert higher effort, achieve higher productivity, have more difficult goals, and pay their CEOs with a higher portion of fixed income. We also find that highly round gross margins are associated with superior performance. Additionally, we do not find consistent evidence that highly round gross margin reference points are linked to external rewards. Collectively, our evidence is consistent with reference-dependent preferences for highly round gross margins likely being driven by intrinsic (rather than extrinsic) motivations.

报告毛利率的整数参考点和不规则模式

摘要我们发现公司报告的季度毛利率百分比分布不规律。具体来说,与反事实分布预测的结果相比,在高度四舍五入(例如,10的倍数,例如30%,40%等)或整齐可除(例如,25%,75%)的百分比整数周围存在显著的聚集。进一步的调查显示,高圆整毛利率的公司规模较小,付出的努力更大,实现的生产率更高,目标更困难,并且支付给ceo的固定收益比例更高。我们还发现,高圆整的毛利率与卓越的业绩有关。此外,我们没有发现一致的证据表明,高度圆整的毛利率参考点与外部奖励有关。总的来说,我们的证据与对高圆整毛利率的参考依赖偏好是一致的,这种偏好可能是由内在(而不是外在)动机驱动的。

本文章由计算机程序翻译,如有差异,请以英文原文为准。

求助全文

约1分钟内获得全文

求助全文

来源期刊

Review of Accounting Studies

BUSINESS, FINANCE-

CiteScore

7.90

自引率

7.10%

发文量

82

期刊介绍:

Review of Accounting Studies provides an outlet for significant academic research in accounting including theoretical, empirical, and experimental work. The journal is committed to the principle that distinctive scholarship is rigorous. While the editors encourage all forms of research, it must contribute to the discipline of accounting. The Review of Accounting Studies is committed to prompt turnaround on the manuscripts it receives. For the majority of manuscripts the journal will make an accept-reject decision on the first round. Authors will be provided the opportunity to revise accepted manuscripts in response to reviewer and editor comments; however, discretion over such manuscripts resides principally with the authors. An editorial revise and resubmit decision is reserved for new submissions which are not acceptable in their current version, but for which the editor sees a clear path of changes which would make the manuscript publishable. Officially cited as: Rev Account Stud

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: