Listed Real Estate as an Inflation Hedge Across Regimes

The Journal of Real Estate Finance and Economics

Pub Date : 2023-10-16

DOI:10.1007/s11146-023-09964-x

引用次数: 0

Abstract

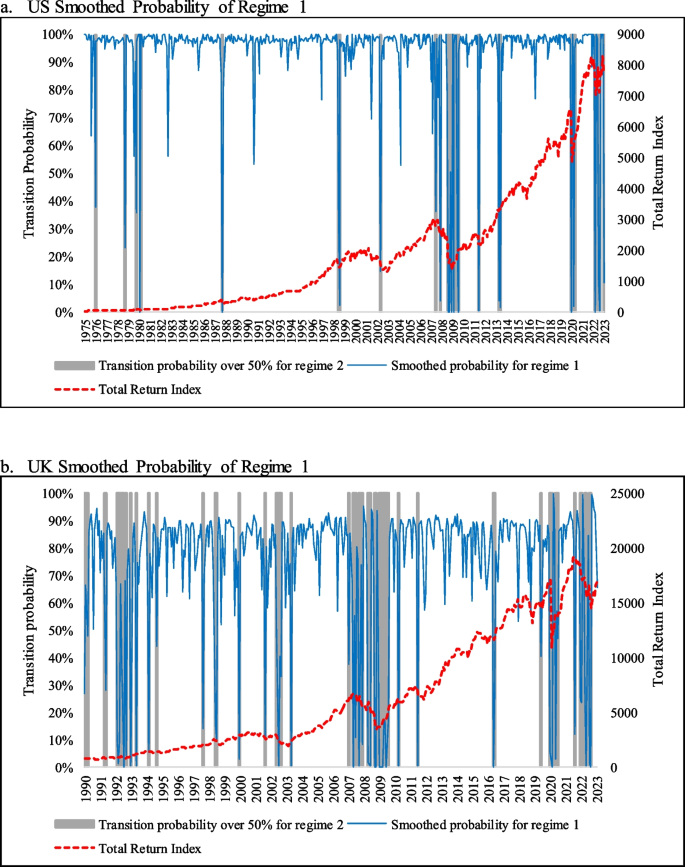

Abstract This paper examines the inflation-hedging capability of listed real estate (LRE) companies in the US from 1975 to 2023, and in three other economies—the UK, Japan, and Australia—from 1990 to 2023. By using a Markov switching vector error correction model (MS-VECM), we identify that the short-term hedging ability moves towards being negative or zero during turbulent periods. In stable periods, LRE provides good protection against inflation. In the long term, LRE offers a good hedge against expected inflation and shows a superior inflation hedging ability than stocks. Additionally, we identify inflation-hedging portfolios by minimizing the expected shortfall. This inflation-hedging portfolio allocation methodology suggests that listed real estate stocks should play a significant role in investor portfolios.

将房地产作为跨制度的通货膨胀对冲

摘要本文考察了1975年至2023年美国房地产上市公司的通胀对冲能力,以及1990年至2023年英国、日本和澳大利亚房地产上市公司的通胀对冲能力。通过使用马尔可夫切换向量误差修正模型(MS-VECM),我们发现短期对冲能力在动荡时期趋向于负或零。在稳定时期,LRE可以很好地防范通货膨胀。从长期来看,LRE可以很好地对冲预期的通胀,并显示出比股票更好的通胀对冲能力。此外,我们通过最小化预期缺口来确定通胀对冲投资组合。这种对冲通胀的投资组合配置方法表明,上市地产股应该在投资者的投资组合中发挥重要作用。

本文章由计算机程序翻译,如有差异,请以英文原文为准。

求助全文

约1分钟内获得全文

求助全文

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: