Systemic Risk in Indian Financial Institutions: A Probabilistic Approach

Abstract

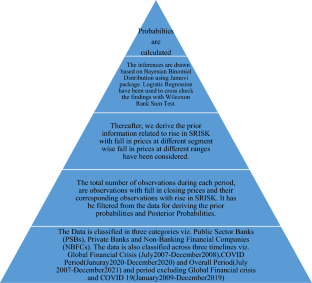

In this paper, we have carried out the predictions for growth or spurt in Systemic Risk across the different categories of financial institutions in India relative to the change in the market prices. We have used Bayes Theorem along with Logistic regressions to work out the actual probabilities regarding the growth in Systemic Risk with the fall in stock prices and Wilcoxon Rank sum Test to validate the robustness of the models. In this paper, we have studied the period from July 2007 to December 2020. An important feature observed was any fall in closing prices beyond 30%, is contributing for 90% growth in systemic risk. A policy implication can follow—that it is imperative to monitor a sharp decline in market prices to the tune of 30% or more by regulators to avoid a crisis. We generally presume that state ownership of Banks particularly in India generates public confidence. Our paper has been able to support the theory of public confidence wherein the Public Sector Banks are contributing less towards the growth of Systemic Risk as compared to Private Banks and NBFCs. The NBFCs are the highest contributor of the growth in systemic risk which we have differentiated from our results. So, in coming days NBFCs are to be closely monitored by the regulators and suitable regulatory measures need to be placed.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: